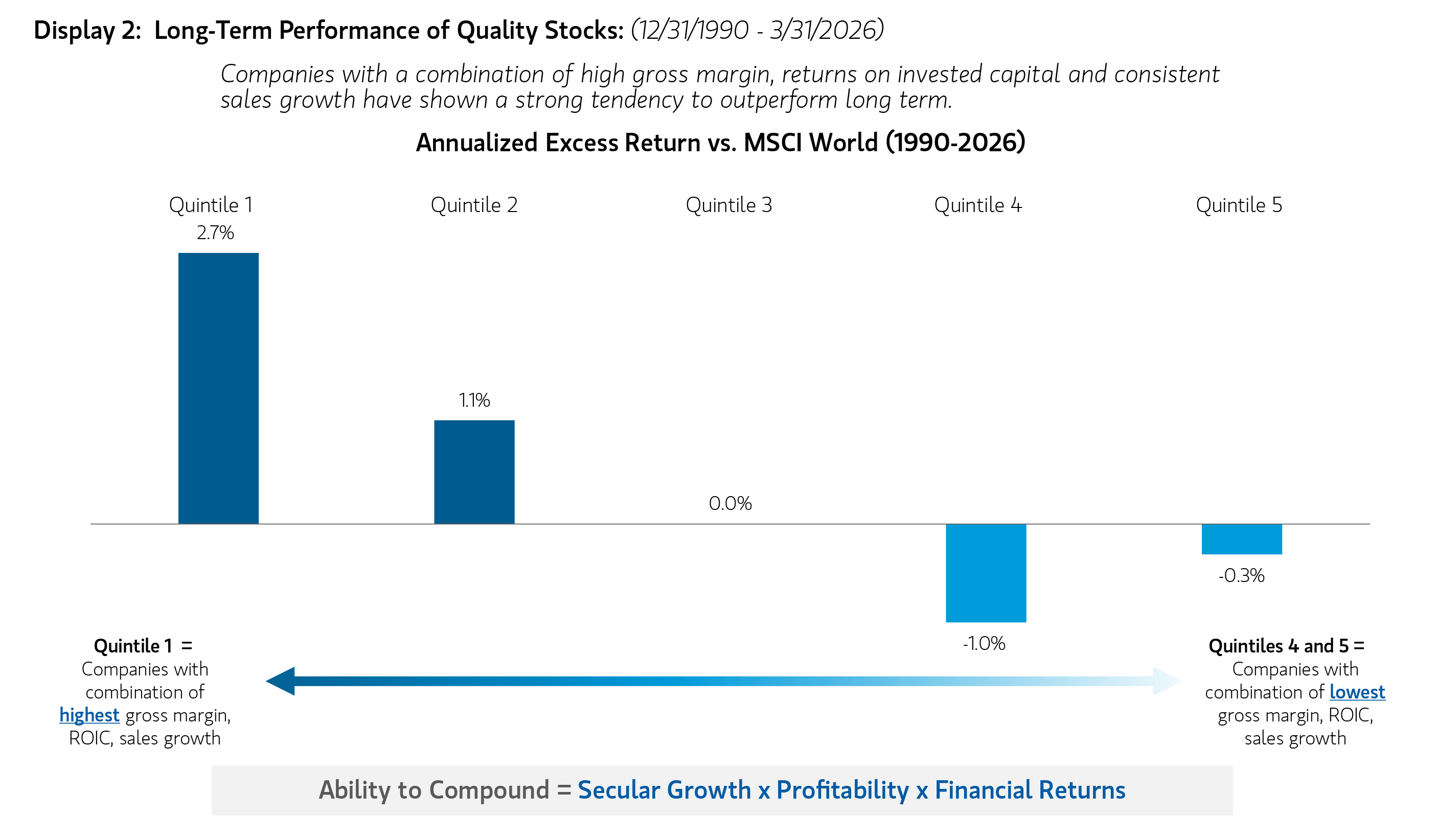

After several years of lagging market leadership, quality-oriented equities may offer an attractive entry point for long-term investors. Historically, companies with durable business models, strong returns on capital, disciplined capital allocation and resilient competitive positions have generated disproportionate shareholder value over time (Display 2). Their ability to create sustainable cash flows and compound earnings across market cycles has been a key driver of that long-term performance, while potentially providing resilience during periods of economic stress.

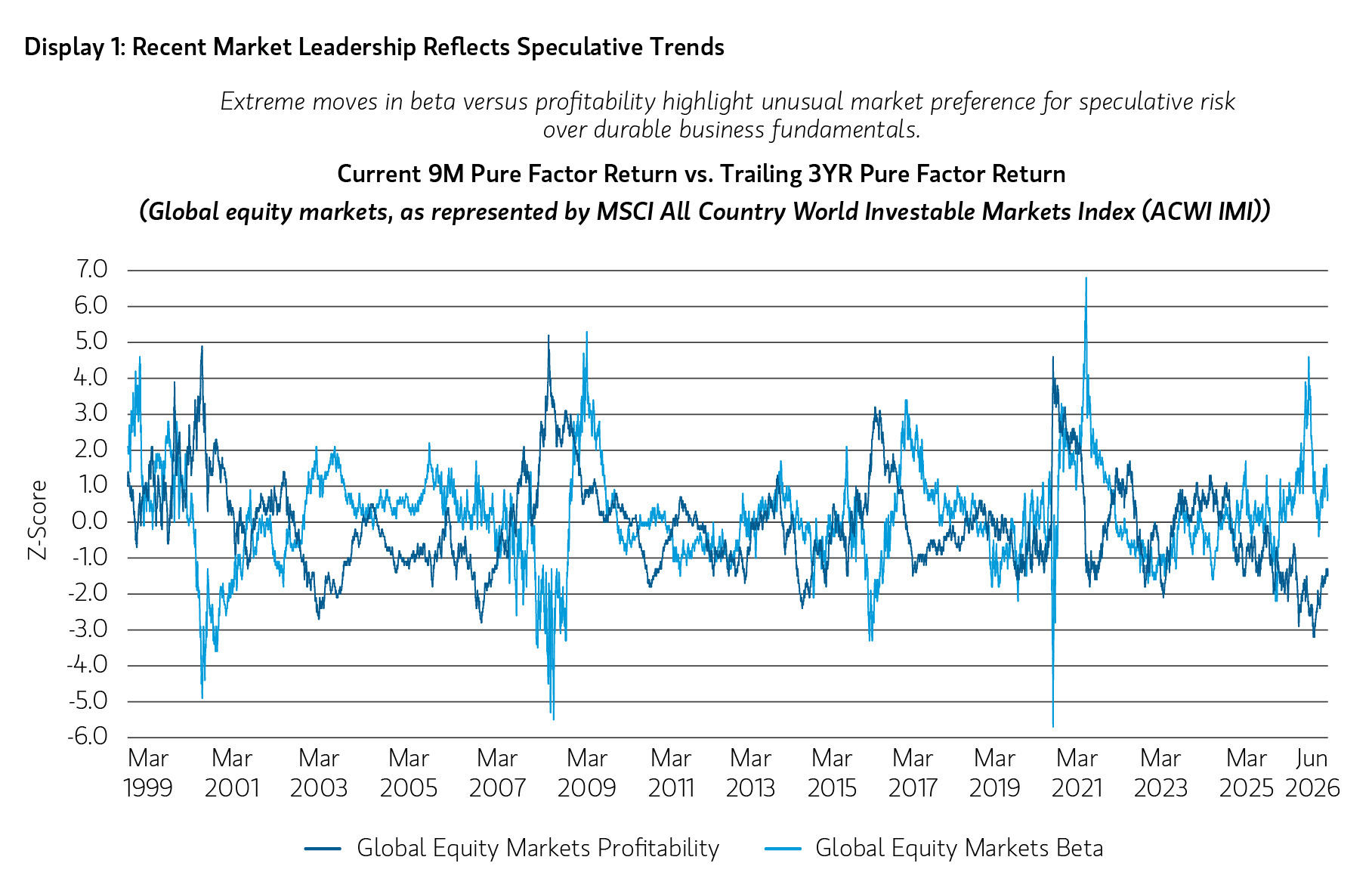

Yet quality-oriented factors have been notably out of favor in recent years. Market leadership has become increasingly concentrated in companies tied to artificial intelligence, digital infrastructure and other high-growth themes. As investors have prioritized future growth potential, traditional measures of quality, such as profitability and balance-sheet strength, have played a diminished role in market leadership. Recent factor behavior illustrates the extent of this divergence.

The Z score is representative of returns. It is a statistical measurement that describes a value’s relationship to the mean of a group cohorts. Z score is measured in terms of standard deviations from the mean. Profitability is a composite of four equal-weighted descriptors designed to measure how efficiently a firm’s operations generate profits. Beta explains common variations in stock returns due to different stock sensitivities to market systemic risk that cannot be explained by the World factor. World factor is from FactSet and the market beta used in our risk models.

Source: FactSet, Barra as of April 16, 2026. Data provided for informational purposes only. Past performance is no guarantee of future returns. It is not possible to invest directly in an index.

In global equity markets, investor risk appetite reached unusually elevated levels during the recent market cycle, from Q1 2025 to present, while profitability-oriented factors experienced historically weak performance. This divergence reflects an environment in which investors increasingly prioritized future growth expectations over current profitability and business durability.

Periods like this are not unprecedented. Market history is filled with episodes in which investor enthusiasm temporarily outweighs business fundamentals. During these periods, quality investing can appear frustratingly out of sync with prevailing market leadership. Over time, however, fundamentals have consistently reasserted themselves.

The reason is straightforward: business fundamentals matter. Companies that generate sustainable free cash flow, maintain strong competitive positions and allocate capital effectively are generally better equipped to navigate economic uncertainty, changing competitive dynamics and periods of market volatility. Empirical evidence across developed equity markets, shown in Display 2, supports this view.

Long-term evidence

We have found that companies within the MSCI World Index that combine high sales growth, strong margins and attractive returns on invested capital consistently outperformed over multiyear periods. Notably, these companies also tended to exhibit lower volatility than many lower-quality peers, highlighting the potential benefits of quality across both return and risk dimensions.

Source: Eaton Vance, FactSet and Barra. As of 3/31/2026. Study ran for the period of 12/31/1990 to 3/31/2026, based on the holdings in the MSCI World Index. The MSCI World Index was broken into 5 quintiles, defined by equally weighted factors (sales growth, gross margin and return on invested capital (ROIC). Quintile 1 was populated with companies demonstrating the highest combination of sales growth, gross margin and ROIC, while Quintile 5 represented companies with the lowest combination. These quintile groupings were held for 5 years. A new quintile grouping was created every subsequent month and held for 5 years. The quintiles in the above graph represent the market-weighted excess return of the combined groupings for each quintile over the full time period. Past performance is no guarantee of future returns. It is not possible to invest directly in an index.

Why quality may be attractive today

The case for quality may become even stronger in the years ahead. A higher cost-of-capital environment, increasing geopolitical uncertainty, and greater economic fragmentation may create advantages for businesses with strong balance sheets, pricing power, and the ability to fund growth internally. At the same time, recent market dynamics have created an unusual valuation backdrop. While investors historically have been willing to pay premium valuations for quality businesses, many now trade at more reasonable valuations, despite improving fundamentals.

As profitability has improved across portions of the quality universe, relative valuations have compressed. The result is a potentially compelling combination of stronger business fundamentals and lower relative expectations. In some areas of the market, high-quality businesses appear unusually inexpensive relative to their long-term earnings power and competitive strength.

The investment case for quality therefore extends beyond the enduring strengths of these businesses. It also reflects the possibility that today’s market offers an attractive entry point into quality companies, as improving fundamentals have not been fully recognized in valuations.

Conclusion

In our view, it’s clear that while quality investing may remain challenged over shorter periods, the underlying principles remain intact. Decades of empirical evidence suggest to us that businesses with durable competitive advantages and strong fundamentals have consistently created value over time.

We believe successful, long-term investing is not about chasing the strongest 12-month performance trend. It is about owning businesses capable of creating value across a full market cycle and maintaining conviction when market leadership shifts.

Innovation matters. Narratives matter. But over the long term, business fundamentals matter most.

Featured Insights

Index definitions:

MSCI All Country World Investable Markets Index (ACWI IMI) captures large, mid and small cap representation across 23 Developed Markets and 24 Emerging Markets countries. The index is comprehensive, covering approximately 99% of the global equity investment opportunity set.

MSCI World Index is a free float‑adjusted, market capitalization weighted index designed to measure the performance of developed equity markets globally.

Risk Considerations:

The value of investments held by the Strategy may increase or decrease in response to economic, and financial events (whether real, expected or perceived) in the U.S. and global markets. The value of equity securities is sensitive to stock market volatility. Investing primarily in responsible investments carries the risk that, under certain market conditions, the Strategy may underperform funds that do not utilize a responsible investment strategy. The Strategy is exposed to liquidity risk when trading volume, lack of a market maker or trading partner, large position size, market conditions, or legal restrictions impair its ability to sell particular investments or to sell them at advantageous market prices. The impact of the coronavirus on global markets could last for an extended period and could adversely affect the Strategy’s performance.

The views and opinions and/or analysis expressed are those of the author or the investment team as of the date of preparation of this material and are subject to change at any time without notice due to market or economic conditions and may not necessarily come to pass. Furthermore, the views will not be updated or otherwise revised to reflect information that subsequently becomes available or circumstances existing, or changes occurring, after the date of publication. The views expressed do not reflect the opinions of all investment personnel at Morgan Stanley Investment Management (MSIM) and its subsidiaries and affiliates (collectively “the Firm”) and may not be reflected in all the strategies and products that the Firm offers.

Forecasts and/or estimates provided herein are subject to change and may not actually come to pass. Information regarding expected market returns and market outlooks is based on the research, analysis and opinions of the authors or the investment team. These conclusions are speculative in nature, may not come to pass and are not intended to predict the future performance of any specific strategy or product the Firm offers. Future results may differ significantly depending on factors such as changes in securities or financial markets or general economic conditions.

This material has been prepared on the basis of publicly available information, internally developed data and other third-party sources believed to be reliable. However, no assurances are provided regarding the reliability of such information and the Firm has not sought to independently verify information taken from public and third-party sources.

This material is a general communication, which is not impartial, is for informational and educational purposes only, not a recommendation to purchase or sell specific securities, or to adopt any particular investment strategy. Information does not address financial objectives, situation or specific needs of individual investors.

Any charts and graphs provided are for illustrative purposes only.

This material is not a product of Morgan Stanley’s Research Department and should not be regarded as a research material or a recommendation.

The Firm has not authorised financial intermediaries to use and to distribute this material, unless such use and distribution is made in accordance with applicable law and regulation. Additionally, financial intermediaries are required to satisfy themselves that the information in this material is appropriate for any person to whom they provide this material in view of that person’s circumstances and purpose. The Firm shall not be liable for, and accepts no liability for, the use or misuse of this material by any such financial intermediary.

This material may be translated into other languages. Where such a translation is made this English version remains definitive. If there are any discrepancies between the English version and any version of this material in another language, the English version shall prevail.

The whole or any part of this material may not be directly or indirectly reproduced, copied, modified, used to create a derivative work, performed, displayed, published, posted, licensed, framed, distributed or transmitted or any of its contents disclosed to third parties without the Firm’s express written consent. This material may not be linked to unless such hyperlink is for personal and non-commercial use. All information contained herein is proprietary and is protected under copyright and other applicable law.

DISTRIBUTION

This material is only intended for and will only be distributed to persons resident in jurisdictions where such distribution or availability would not be contrary to local laws or regulations.

MSIM, the asset management division of Morgan Stanley (NYSE: MS), and its affiliates have arrangements in place to market each other’s products and services. Each MSIM affiliate is regulated as appropriate in the jurisdiction it operates. MSIM’s affiliates are: Calvert Research and Management, Eaton Vance Management, Parametric Portfolio Associates LLC, Parametric SAS, and Atlanta Capital Management LLC.

This material has been issued by any one or more of the following entities:

EMEA

This material is for Professional Clients/Accredited Investors only.

In the EU, MSIM materials are issued by MSIM Fund Management (Ireland) Limited (“FMIL”). FMIL is regulated by the Central Bank of Ireland and is incorporated in Ireland as a private company limited by shares with company registration number 616661 and has its registered address at 24-26 City Quay, Dublin 2, DO2 NY19, Ireland.

Outside the EU, MSIM materials are issued by Morgan Stanley Investment Management Limited (MSIM Ltd) is authorised and regulated by the Financial Conduct Authority. Registered in England. Registered No. 1981121. Registered Office: 25 Cabot Square, Canary Wharf, London E14 4QA.

In Switzerland, MSIM materials are issued by Morgan Stanley & Co. International plc, London (Zurich Branch) Authorised and regulated by the Eidgenössische Finanzmarktaufsicht ("FINMA"). Registered Office: Beethovenstrasse 33, 8002 Zurich, Switzerland.

Italy: MSIM FMIL (Milan Branch), (Sede Secondaria di Milano) Palazzo Serbelloni Corso Venezia, 16 20121 Milano, Italy. The Netherlands: MSIM FMIL (Amsterdam Branch), Rembrandt Tower, 11th Floor Amstelplein 1 1096HA, Netherlands. France: MSIM FMIL (Paris Branch), 61 rue de Monceau 75008 Paris, France. Spain: MSIM FMIL (Madrid Branch), Calle Serrano 55, 28006, Madrid, Spain. Germany: MSIM FMIL Frankfurt Branch, Große Gallusstraße 18, 60312 Frankfurt am Main, Germany (Gattung: Zweigniederlassung (FDI) gem. § 53b KWG). Denmark: MSIM FMIL (Copenhagen Branch), Gorrissen Federspiel, Axel Towers, Axeltorv2, 1609 Copenhagen V, Denmark.

MIDDLE EAST

Dubai International Financial Centre: This information does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe for or purchase, any securities or investment products in the UAE (including the Dubai International Financial Centre and the Abu Dhabi Global Market) and accordingly should not be construed as such. Furthermore, this information is being made available on the basis that the recipient acknowledges and understands that the entities and securities to which it may relate have not been approved, licensed by or registered with the UAE Central Bank, the Dubai Financial Services Authority, the UAE Securities and Commodities Authority, the Financial Services Regulatory Authority or any other relevant licensing authority or government agency in the UAE. The content of this report has not been approved by or filed with the UAE Central Bank, the Dubai Financial Services Authority, the UAE Securities and Commodities Authority or the Financial Services Regulatory Authority.

Abu Dhabi Global Market ("ADGM"): This material is sent strictly within the context of, and constitutes, an Exempt Communication. This material relates to emerging markets debt, which is not subject to any form of regulation or approval by the Financial Services Regulatory Authority of the Abu Dhabi Global Market (the “FSRA”).

Saudi Arabia

This financial promotion was issued and approved for use in Saudi Arabia by Morgan Stanley Saudi Arabia, Al Rashid Tower, Kings Sand Street, Riyadh, Saudi Arabia, authorized and regulated by the Capital Market Authority license number 06044-37.

U.S.

NOT FDIC INSURED | OFFER NO BANK GUARANTEE | MAY LOSE VALUE | NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY | NOT A DEPOSIT

Latin America (Brazil, Chile Colombia, Mexico, Peru, and Uruguay)

This material is for use with an institutional investor or a qualified investor only. All information contained herein is confidential and is for the exclusive use and review of the intended addressee, and may not be passed on to any third party. This material is provided for informational purposes only and does not constitute a public offering, solicitation or recommendation to buy or sell for any product, service, security and/or strategy. A decision to invest should only be made after reading the strategy documentation and conducting in-depth and independent due diligence.

ASIA PACIFIC

Hong Kong: This document has been issued by Morgan Stanley Asia Limited, CE No. AAD291, for use in Hong Kong and shall only be made available to “professional investors” as defined under the Securities and Futures Ordinance of Hong Kong (Cap 571). The contents of this document have not been reviewed nor approved by any regulatory authority including the Securities and Futures Commission in Hong Kong. Accordingly, save where an exemption is available under the relevant law, this document shall not be issued, circulated, distributed, directed at, or made available to, the public in Hong Kong. Singapore: This material is disseminated in Singapore by Morgan Stanley Investment Management Company, Registration No. 199002743C. This material should not be considered to be the subject of an invitation for subscription or purchase, whether directly or indirectly, to the public or any member of the public in Singapore other than (i) to an institutional investor under section 304 of the Securities and Futures Act, Chapter 289 of Singapore (“SFA”), (ii) to a “relevant person” (which includes an accredited investor) pursuant to section 305 of the SFA, and such distribution is in accordance with the conditions specified in section 305 of the SFA; or (iii) otherwise pursuant to, and in accordance with the conditions of, any other applicable provision of the SFA. This material has not been reviewed by the Monetary Authority of Singapore. Australia: This material is provided by Morgan Stanley Investment Management (Australia) Pty Ltd ABN 22122040037, AFSL No. 314182 and its affiliates and does not constitute an offer of interests. Morgan Stanley Investment Management (Australia) Pty Limited arranges for MSIM affiliates to provide financial services to Australian wholesale clients. This material will not be lodged with the Australian Securities and Investments Commission.

Japan

For professional investors, this material is circulated or distributed solely for informational purposes. For non-professional investors, this material is provided in connection with Morgan Stanley Investment Management (Japan) Co., Ltd. (“MSIMJ”)’s business with respect to discretionary investment management agreements (“IMA”) and investment advisory agreements (“IAA”). This does not constitute a recommendation or solicitation of transactions nor offers any particular financial instruments. Under an IMA, with respect to the management of client assets, the client prescribes basic management policies in advance and commissions MSIMJ to make all investment decisions based on an analysis of the value, etc. of the securities, and MSIMJ accepts such commission. The client shall delegate to MSIMJ the authorities necessary to make such investment decisions. MSIMJ exercises these delegated authorities accordingly, and the client shall not make individual instructions. All investment profits and losses belong to the clients; principal is not guaranteed. Please consider the investment objectives and nature of risks before investing. As an investment advisory fee for an IAA or an IMA, the amount of assets subject to the contract multiplied by a certain rate (the upper limit is 2.20% per annum (including tax)) shall be incurred in proportion to the contract period. For some strategies, a contingency fee may be incurred in addition to the fee mentioned above. Indirect charges also may be incurred, such as brokerage commissions for underlying securities. Since these charges and expenses vary by contract and other factors, MSIMJ cannot present the rates, upper limits, etc. in advance. All clients should read thoroughly the Documents Provided Prior to the Conclusion of a Contract carefully before executing an agreement. This material is distributed in Japan by MSIMJ, Registered No. 410 (Director of Kanto Local Finance Bureau (Financial Instruments Firms)), Membership: the Japan Securities Dealers Association, the Investment Management Association of Japan and the Type II Financial Instruments Firms Association.

© 2026 Morgan Stanley. All rights reserved. RO# 5588710 06/29/2027