A strong business isn’t always a winning stock at every moment, and 2025 was a good reminder of that. Developed market equities finished the year up more than 20%, but quality stocks lagged. That’s why Parametric favors a multifactor approach to capture factor risk premia.

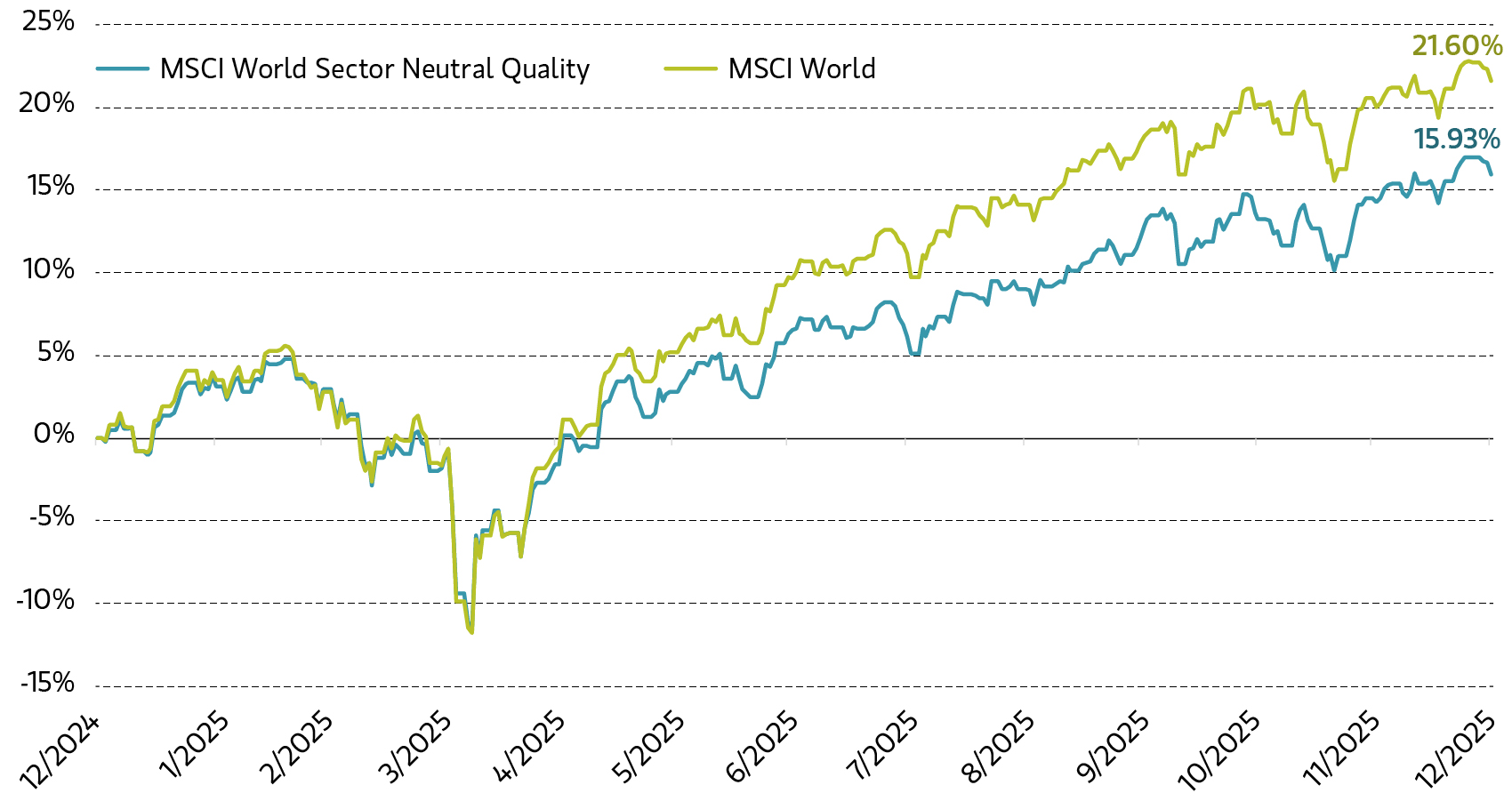

By one common measure, the MSCI World Quality Index returned 16.94% in 2025 versus 21.60% for the MSCI World Index. In MSCI’s sector-neutral framework, which strips out sector weight differences to isolate the factor more cleanly, World quality trailed its parent benchmark by -5.67%.

While disappointing in the short term, this underperformance isn’t unprecedented. Factor returns are inherently cyclical. For investors committed to long-term outcomes, the key is understanding why quality lagged and how a diversified approach to factor investing can help navigate such periods.

What is the quality factor?

The quality factor targets companies with strong fundamentals: high return on equity, low debt and stable earnings—simply put, companies whose underlying businesses are financially healthy. These firms tend to be better positioned to weather economic uncertainty and have historically delivered attractive risk-adjusted returns across market cycles.

In practice, quality is often accessed through indexes like the MSCI World Quality Index or ETFs that track similar metrics. These portfolios typically include large, well-established companies with robust balance sheets and consistent profitability.

Why did quality lag?

From April 2025 through the end of the year, quality stocks trailed the broader market by an increasingly wide margin. While both posted solid gains, quality’s relative performance lagged—particularly in the second half of 2025 following the market volatility around the April 2 tariff announcements in the US.

Quality stocks diverged from the broad equity market after April 2025

Quality stocks diverged from the broad equity market after April 2025

Several dynamics may have contributed to quality’s underperformance for the year:

Low-quality rally. Since bottoming after the “liberation day” announcement in April, so-called junk stocks—high beta, unprofitable and highly speculative companies—underwent a sharp rally as the administration walked back its most extreme tariff proposals and investors became more comfortable with positive trends in the US economy and corporate profits. In contrast, companies with high returns on equity and low leverage delivered single-digit returns.

Unfavorable macro backdrop. Quality stocks have often performed best when economic growth is slowing and interest rates are easing. Investors tend to favor stable, resilient businesses in those periods. In 2025, the environment looked different. Growth stayed relatively firm, which generally created a better backdrop for other parts of the market than for quality stocks.

Rotation to other factors. While quality struggled, other factors such as momentum, size and beta fared better. Many of the larger AI-centric companies outperformed, resulting in a continuation of themes well underway in the market.

It’s important to remember that no factor outperforms in every environment. Quality’s recent underperformance isn’t a sign of structural weakness, but rather a reflection of the natural ebb and flow of factor returns.

Historical data has supported this view. Over the last quarter century, following one-year periods when quality underperformed the market (using the same MSCI indexes), the factor went on to outperform over the subsequent three-year period 77% of the time.

A multifactor approach for all seasons

At Parametric, we believe that the best way to capture factor risk premia is through a diversified, risk-managed multifactor strategy. Our approach targets four core investment themes—quality, value, momentum and low volatility—each supported by academic research and our proprietary insights.

Our multifactor strategy is designed to manage factor cyclicality through:

Integrated optimization

Rather than blending single-factor portfolios, we construct a unified portfolio that considers all factor exposures, risk constraints and liquidity limits simultaneously. We believe that this helps avoid unintended bets, such as sector or style tilts, that can dilute performance.

Dynamic factor timing

We monitor the recent risk-adjusted performance of each factor and adjust exposures accordingly. When a factor like quality underperforms or becomes more volatile, we trim the exposure to it. Conversely, we lean into factors with stronger momentum. This disciplined rebalancing helps manage risk and capture emerging opportunities.

Exposure constraints

We limit the contribution of any single factor to the overall risk of the portfolio. This helps ensure that no one factor dominates performance, reducing the impact of short-term underperformance.

Full market exposure

Our portfolios are constructed with a target beta of 1.0, ensuring full participation in equity market returns. This helps avoid the low-beta drag that can affect some multifactor strategies.

The bottom line

Years like 2025 can test investor conviction, but abandoning a factor strategy after a period of underperformance risks missing the rebound—look no further than this year for evidence of that. In the first quarter, the MSCI World Sector Neutral Quality index outperformed the broad MSCI World market by 1.21%.

We remain confident in the long-term potential of the quality factor, and in the value of a diversified, risk-aware approach to factor investing. Using a multifactor approach can help to deliver a more consistent path to long-term performance by smoothing the ride and reducing reliance on any single factor. For investors seeking to navigate uncertain markets without making tactical bets, a thoughtfully constructed multifactor strategy may offer a compelling solution.

Featured Insights