Each June, the Russell Index Reconstitution quietly reshapes the U.S. equity landscape. While it rarely generates headlines outside institutional circles, it can have meaningful implications for portfolio positioning, passive fund flows and investor rebalancing. This year's changes are particularly noteworthy across several equity segments.

While the changes to Russell Indexes will not take effect until June 26, 2026, FTSE Russell has released preliminary data that allows us to estimate their magnitude. The process systematically evolves the indexes—against which trillions of dollars are managed—to better reflect the investment universe. It involves redistributing companies by both market capitalization and style (growth versus value), as highlighted below.

Market Capitalization Reset

FTSE Russell is well known for its market capitalization indexes, which serve as benchmarks for large-cap, mid-cap, small-cap, and micro-cap strategies and portfolios. With the Russell 3000 Index up 29% over the 12 months through May, many companies have seen significant shifts in market capitalization and may no longer fit their current index assignments. According to FTSE Russell, the maximum cutoff for the small-cap Russell 2000 Index will be $5.7 billion. As of the end of May, 45 companies in the Russell 2000 Index had market capitalizations above $10 billion, and seven exceeded $20 billion, including Bloom Energy at $81 billion. In addition, the maximum for the Russell Mid-Cap Index will be set at $61.7 billion.

The Growth-Value Divide Blurs

For investors accustomed to viewing growth and value as distinct styles, this year’s reconstitution reinforces that today's market leaders no longer fit neatly within this framework, with many stocks no longer clearly aligned to a single style.

Historically, growth stocks have traded at premium valuations and delivered higher revenue and earnings growth, while value stocks have been viewed as more mature businesses trading at lower valuation multiples.

This year’s reconstitution highlights that many of the market's largest companies now exhibit characteristics of both styles, while others are seeing their business prospects and valuations reshaped by the artificial intelligence buildout. Many investors continue to view mega-cap technology companies as purely growth exposures. Yet many of these firms now pay dividends and no longer trade at stretched valuations. Meanwhile, some previously cyclical, low-valuation companies are experiencing rapid growth driven by AI infrastructure buildout.

The Magnificent Seven: No Longer Pure Growth

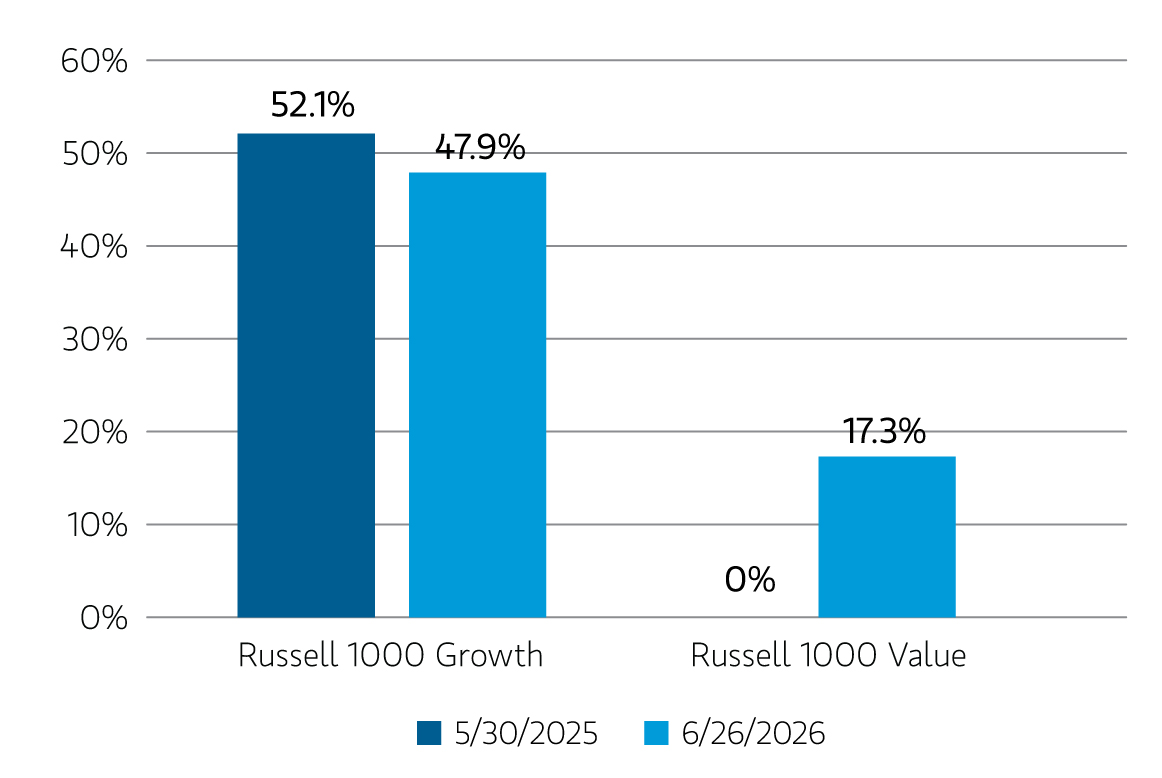

Perhaps the most significant takeaway from this year's reconstitution is that the Magnificent Seven (Apple, Microsoft, Amazon, Alphabet, Meta, NVIDIA and Tesla) are increasingly difficult to characterize as purely growth-oriented investments.

The June 2025 reconstitution began this trend, as minority portions of Amazon.com, Meta Platforms, and Alphabet were added to the Russell 1000 Value Index. This year, however, that trend has accelerated, with the Russell 1000 Value Index now holding meaningful weights in traditionally prominent “growth stocks.” Investors allocating separately to growth and value strategies may find that they own many of the same companies across both exposures.

Microsoft and Apple have shifted from exclusively Growth Index constituents to top-six holdings in both Growth and Value indexes, while Amazon is expected to be the largest holding in the Russell 1000 Value Index after previously being almost exclusively in Growth. By contrast, Alphabet is expected to move from a small Value allocation to fully allocated to the Growth Index. The expected post-reconstitution allocation of the Magnificent Seven is shown below. These stocks are no longer exclusively the domain of growth investors and may see broader adoption among value managers, given their 17% weight in the Russell 1000 Value Index.

Index Weighting of the Magnificent Seven

Index Weighting of the Magnificent Seven

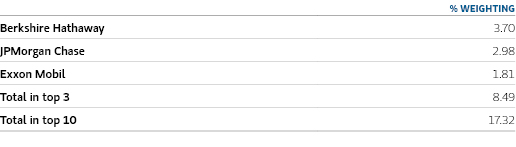

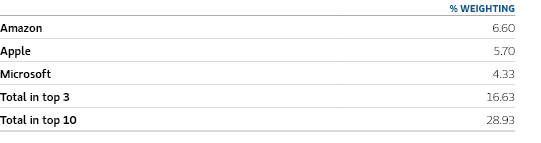

Rising Concentration in the Russell 1000 Value Index

As some of the largest technology companies migrate into the Russell 1000 Value Index, the index is becoming significantly more concentrated in a smaller number of stocks. Investors should recognize that Value Indexes may now behave differently than in the past. Technology-related earnings and market sentiment could exert a greater influence on value performance than in prior cycles.

The largest constituents in the Russell 1000 Value Index represent an increasing share of index weight, meaning a relatively small number of companies can drive a substantial portion of returns. This phenomenon, which has impacted the Russell 1000 Growth and S&P 500 indexes during the last several years, has now spread to the Russell 1000 Value Index.

Russell 1000 Value Index May 31 2025

Russell 1000 Value Index May 31 2025

Russell 1000 Value Index June 26 2026 (pro forma)*

Russell 1000 Value Index June 26 2026 (pro forma)*

In addition, the distinction between broad market exposure and style exposure continues to diminish. As the same mega-cap companies dominate both market-cap-weighted benchmarks and style indexes, portfolio diversification may be less robust than headline allocations suggest.

What This Means for Investors

The Russell reconstitution is more than a technical exercise. It provides a window into how corporate fundamentals and the broader U.S. equity market are evolving. The magnitude of this year’s reconstitution underscores the significant changes taking place. As the line between growth and value continues to blur, it remains critical for investors to evaluate underlying holdings and exposures, and not just their labels or benchmarks. In today's market, understanding underlying holdings matters more than labels or style classifications.

Analyses mises en avant