Targeted Strategies Required for Evolving Demand and Rising Geopolitical Risk

Introduction

2025 marked a stagnant period for commercial real estate. Investors began the year anticipating a rebound after two years of declining values, but global value growth reached only 1.5% through the first three quarters1. Persistent inflation, stoked by tariffs, kept the Fed cautious, resulting in higher-than-expected interest rates, elevated property yields and muted transaction activity. Meanwhile, policy uncertainty slowed occupier decision-making and demand, leaving excess supply—particularly in the U.S.—to pressure rent growth.

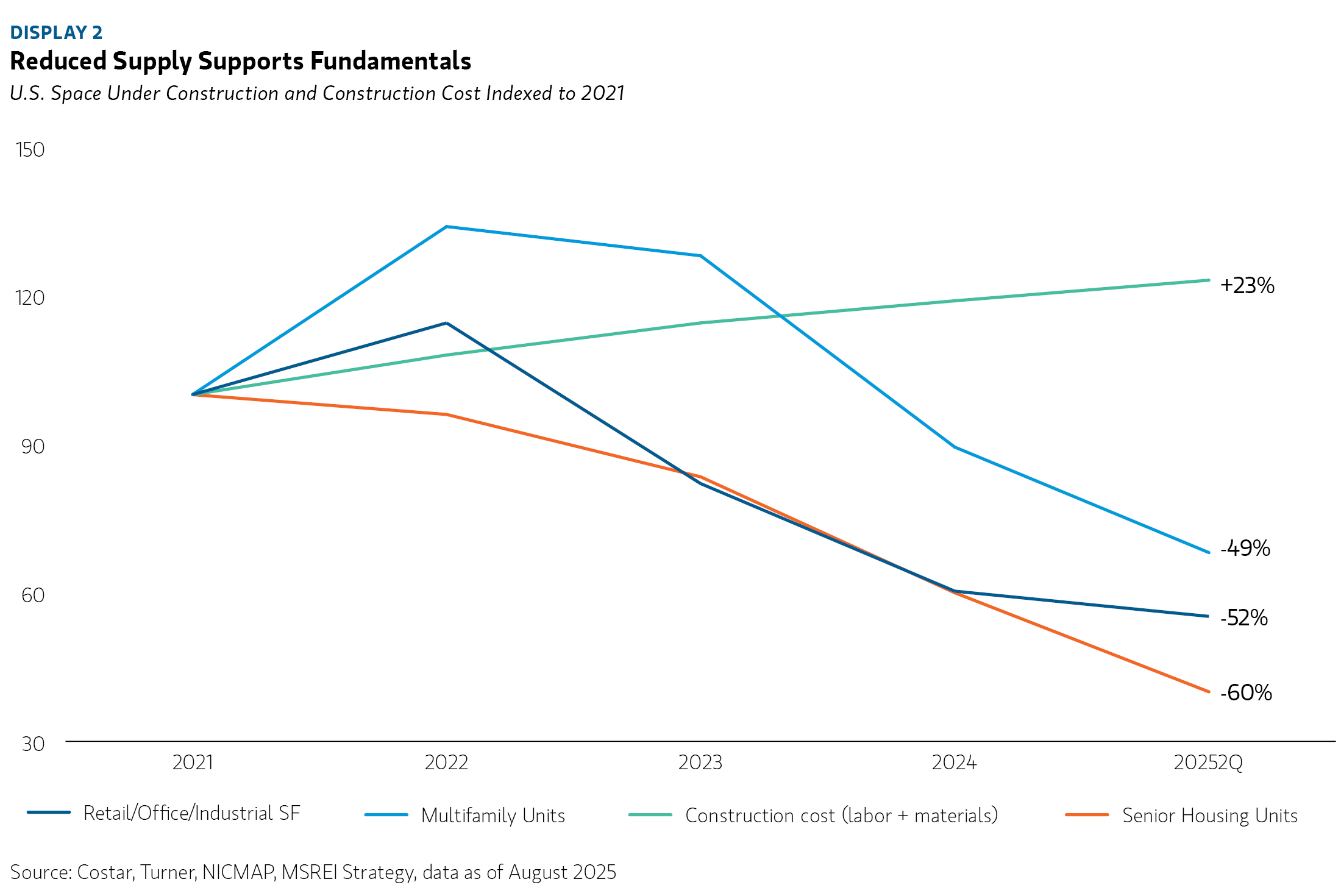

As we enter 2026, the outlook is more constructive. A combination of supportive fiscal and monetary policies, along with deregulation, is fostering procyclical growth across most economies. This backdrop strengthens the investment case for real estate, especially for assets that have repriced by 20–25%. Motivated sellers, engaged buyers, and improved debt availability are setting the stage for a rebound in transactions and valuations. Additionally, the widening gap between rising replacement costs and current market pricing suggests the slowdown in new construction will persist, thus prolonging the next real estate upcycle.

While cyclical recovery will underpin overall market momentum, structural forces are expected to drive greater differentiation in performance. As clarity emerges around demographic shifts, supply chain realignment, and return-to-office trends, occupier preferences are becoming more defined—requiring targeted strategies at the asset, location, and sub-sector levels.

The balance of real estate risks and opportunities is shifting—from elevated macro policy uncertainty to a landscape increasingly defined by rising and more volatile geopolitical risk. In 2025, unpredictable fiscal, monetary, trade, and regulatory policies, particularly in the U.S., contributed to shifting occupier preferences and stagnant demand across several sectors. As we move into 2026, the positive impacts of these policies should become more apparent, supporting more predictable occupier behavior and pockets of strengthening demand.

However, market volatility is expected to remain elevated amid intensifying geopolitical risks and ongoing conflicts in different parts of the world. This evolving risk environment requires investors to adopt a flexible, dynamic, diversified, and highly granular investment approach.

Global Macro Perspective2

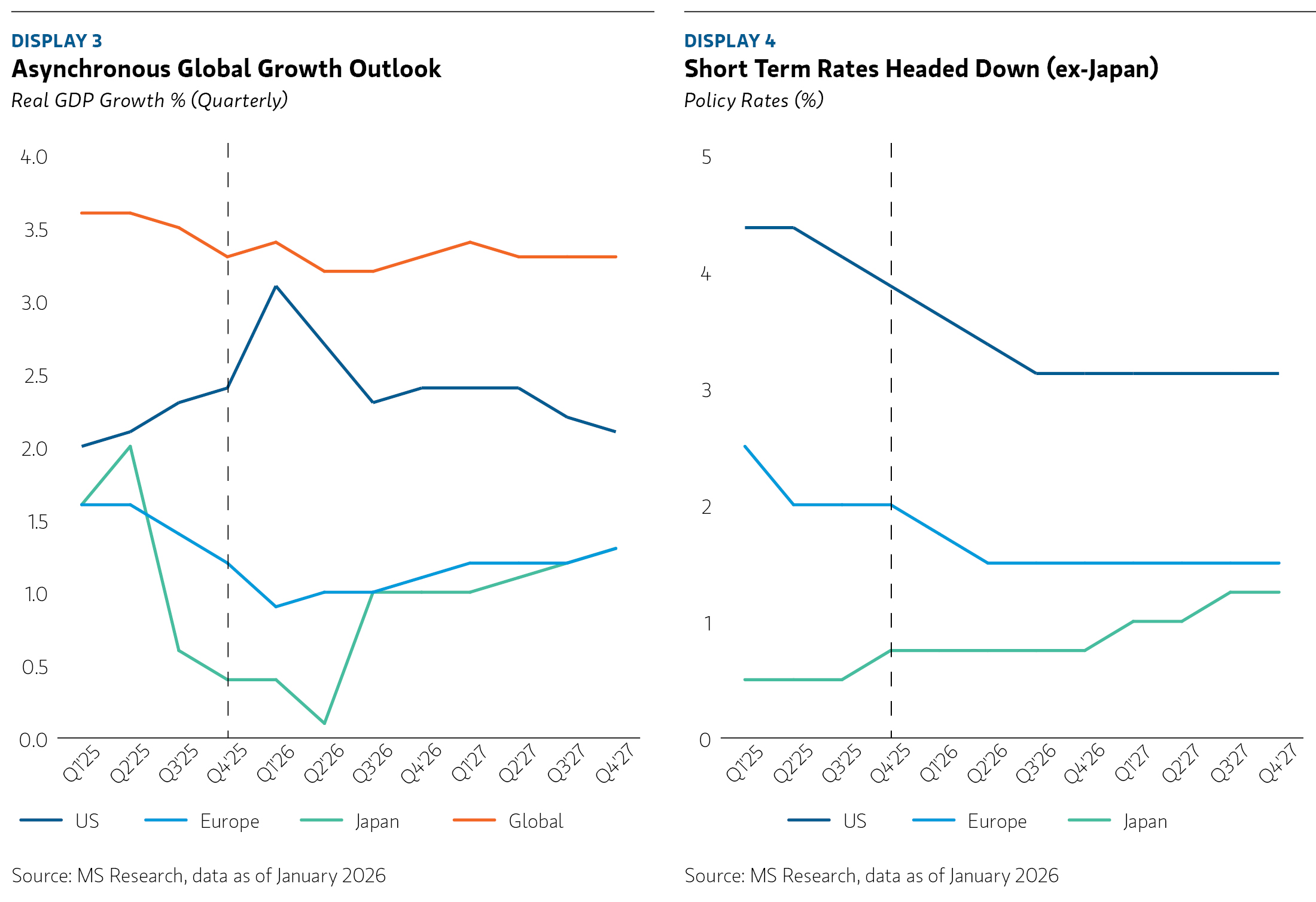

Morgan Stanley Research expects the global economy to moderate through the first half of 2026, then re-accelerate through the end of 2027. However, within this broadly resilient macro backdrop, growth will diverge with the U.S. economy remaining relatively strong, Europe’s growth remaining tepid, Japan and Australia re-accelerating and China’s economy continuing to deflate. Within the U.S., AI-driven capex, resilient high-income consumer spending and improved productivity will lead to faster growth, despite the moderation in job growth. In Europe, growth remains relatively weak in 1H’26 given lower exports and the delay in implementing Germany’s fiscal stimulus. Growth is then expected to reaccelerate in 2H’26 helped by more monetary easing plus rising public spending and a rebound in exports. Japan's GDP growth is expected to remain above trend helped by fiscal stimulus and capital expenditure (government backed high tech investment, tax incentives, and lower energy costs). Lastly, China’s economy remains sluggish, with growth slowing in line with the broader deflationary environment.

Inflation is expected to remain above target in the U.S. as corporates increasingly pass higher tariff costs to the consumer, but assuming that there are no major new tariff announcements, inflation from goods should peak in the first quarter 2026 and then begin to edge down. Inflation in Europe is expected to remain below 2% throughout the forecast period, while in Japan inflation is expected to stay sticky hovering around 2% through YE’27.

Given this broadly slowing inflation trend, interest rates are generally expected to trend lower (excluding Japan), supporting yields and transaction activity. In the U.S., Morgan Stanley Research anticipates an additional 50 bps of cuts after December’s reduction, bringing the terminal rate in 2026 to 3.00–3.25%. Europe is expected to see similar cuts following December’s pause, with a terminal rate of 1.5%. The U.K. and Australia are projected to reduce rates by another 50 bps in 2026. Japan remains an outlier, with policy rates forecast to rise by 50 bps on top of December’s increase, driven by yen depreciation, wage pressures, and fiscal stimulus.

Generally, yield curves are expected to steepen, with long-term bond rates remaining rangebound at today’s elevated levels (vs. pre-COVID) given higher term premiums and fiscal sustainability concerns. This higher interest rate environment requires investment and asset management strategies that prioritize cash flow growth rather than relying on cap rate compression. Accordingly, MSREI will focus on sectors supported by strong structural trends and actively manage assets to enhance value.

MSREI continues to monitor elevated geopolitical risks. Although trade policy uncertainty has eased, rising tensions in Latin America following the U.S. strike on Venezuela — and potential implications for other U.S. allies — remain significant threats. Additionally, heightened U.S. political uncertainty, and conflicts in Ukraine and the Middle East (including Iran’s nuclear trajectory) pose significant global spillover risks.

Global Real Estate Markets

Occupier Fundamentals

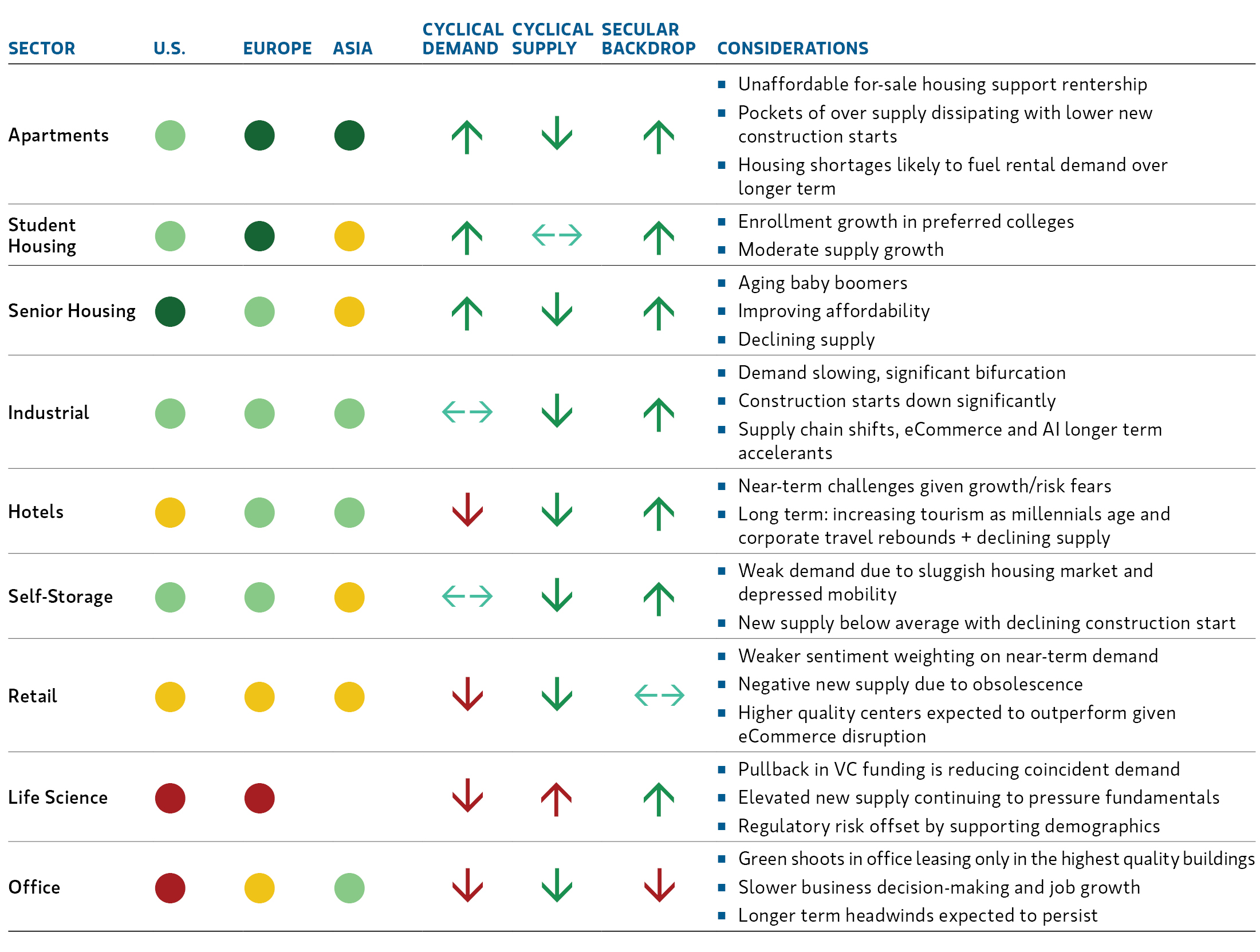

MSREI expects commercial real estate with strong fundamentals to perform well in the current environment, supported by an attractive entry point, lower supply, and alignment with structural demand drivers. The narrative is shifting from supply-driven variability in sector fundamentals to demand bifurcation as the primary performance driver.

Supply, which has been elevated in many asset classes in the U.S., is projected to decline over the next several years as high construction costs and lower rents sustain a wide gap between replacement cost justified rents and market rents, limiting new development. Meanwhile, demand—which has moderated over the past couple of years—is expected to improve, with clear pockets of sector outperformance aligned to structural trends. The impact of these structural shifts on occupier locational and asset-level preferences is becoming clearer. For example, manufacturing is shifting from China to other countries, benefiting different industrial markets and asset types. In residential markets, domestic migration patterns are stabilizing, job growth drivers are shifting and regulatory risks are rising, revealing clearer winners and losers across geographies and asset types. At the same time, the evolution of AI from being an enabling technology to wider spread adoption will likely impact space utilization across many real estate sectors. Technology and defense hubs are also rapidly emerging in each region, supported by onshoring initiatives and increased defense spending. Beyond location, asset-level attributes are becoming more critical differentiators—such as power capacity for industrial properties, amenities for office spaces, grocery anchors for retail, and tailored features for different demographic cohorts for residential assets.

Capital Markets

Market sentiment is generally positive with investors, borrowers and lenders focused on opportunities for deployment and growth. Institutional fundraising is gaining momentum and redemption queues are decreasing, helped by real estate’s relative value versus other asset classes and an increasingly held view that the sector has bottomed and values will rebound consistent with prior cycles.

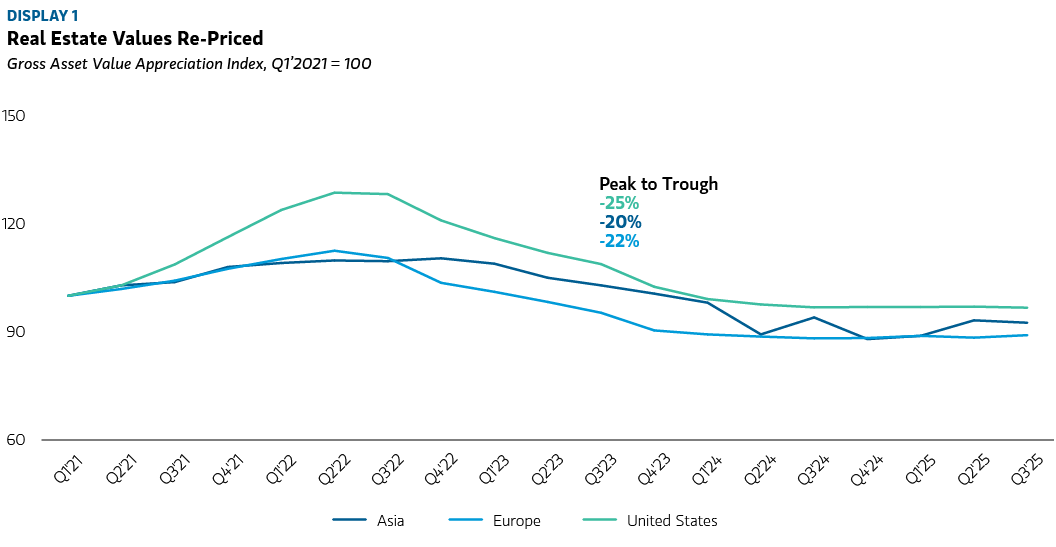

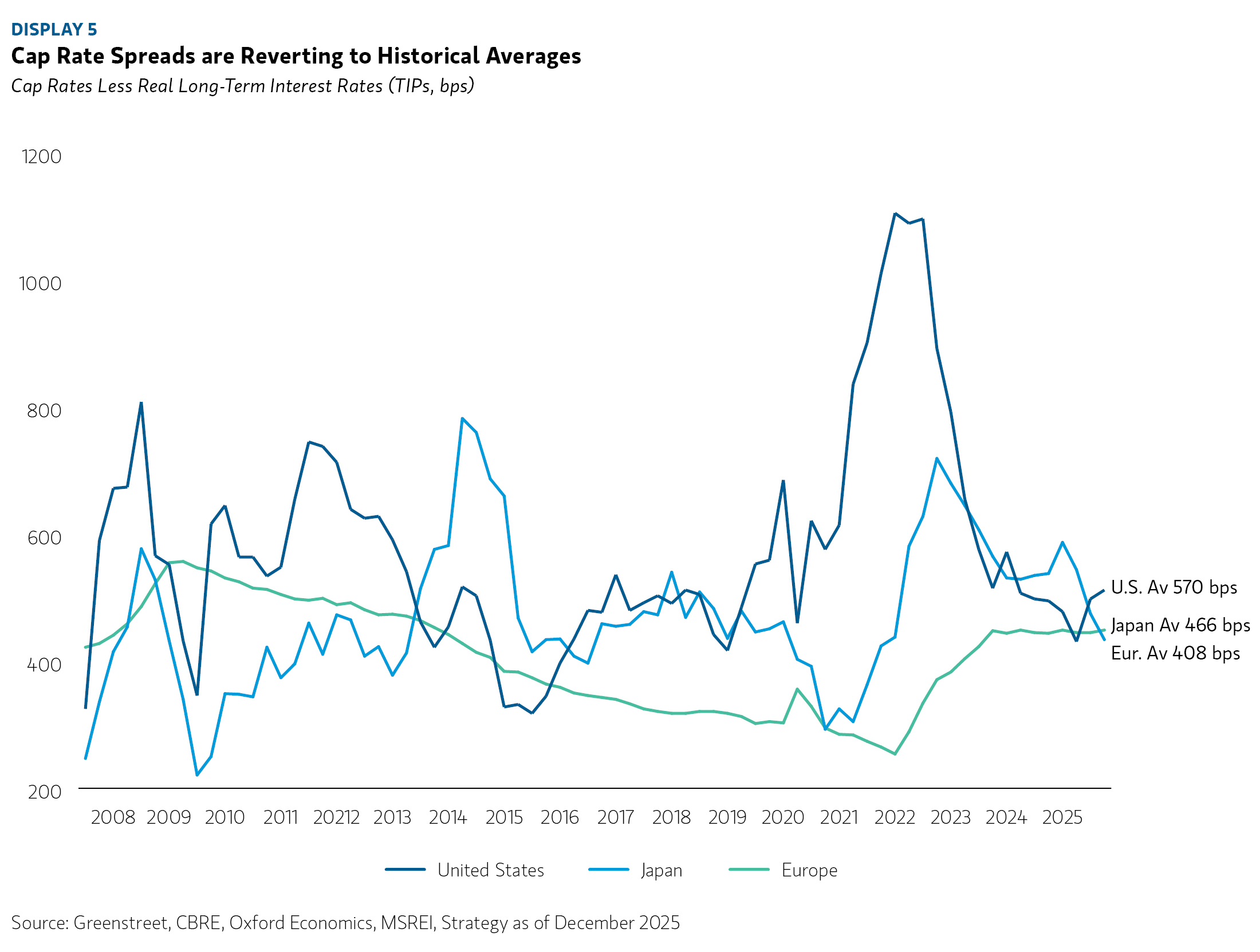

Transaction activity continues to accelerate fueled by active debt markets, with 2025 loan originations on track to reach near record levels in the U.S. Increasing by 16% YOY in the third quarter in the U.S., 25% in Asia Pacific and 6% in Europe3, transaction activity is expected to continue to increase, driven by more motivated sellers and more interested buyers. Owners who have been delaying sales are contending with liquidity needs and maturing debt (with loans coming due between 20252H and 2030 almost double those of the post-GFC cycle, 2010-2014)4. At the same time, buyers are able to price assets at 20-25% below peak5, below replacement cost, and access cheaper, more available and accretive debt. Lower debt margins and falling base rates have normalized real cap rate spreads in the U.S. and Europe back to historical averages6. In Japan, spreads between cap rates and interest rates adjusted for inflation also remain close to historical average levels, but the potential for higher rates and tighter spreads underscores the need for asset-level NOI growth to drive returns.

Sector Fundamentals and Trends

Industrial

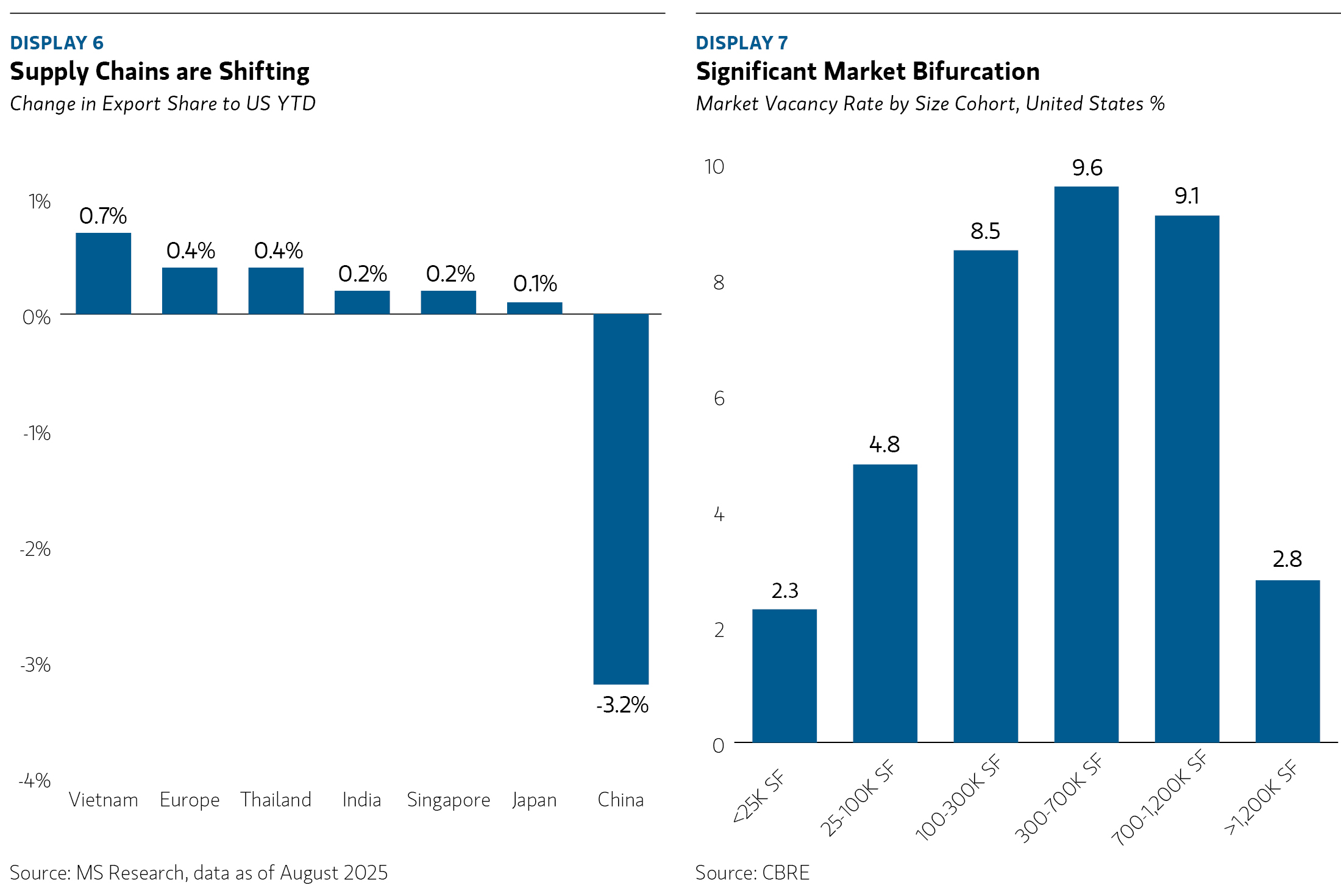

The industrial sector is being reshaped by supply chain realignment, including tariff disruptions, influencing preferred markets and asset types. In the U.S., gross leasing volume for 2025 is projected to be the second highest on record, even as net absorption remains at roughly 60% of normal levels. This can be attributed to consolidation of space requirements, as well as coincidental leasing rollover from the Covid era expansion. Construction starts have declined to levels below pre-COVID norms, with some major markets at 15-year lows. Market rents are >20% below the rents required to justify new construction, creating conditions for rental growth similar to the post-GFC period. Demand is concentrated in cost-efficient markets and size categories, with vacancy rates lowest in small boxes (<25K SF at 2.3%) and large bulk product (>1.2M SF at 2.8%)7.

In Europe, modest macro growth, political uncertainty, greater competition from China and slowing eCommerce penetration have been partially offset by higher defense and technology spending and reshoring initiatives, resulting in slightly lower but uneven take-up in 2025. Germany has seen an increase in demand, supported by fiscal stimulus and defense spending, while Spain’s take-up has also remained elevated helped by strong population and economic growth. Conversely, France’s vacancy rate has doubled over the past 18 months amid political and trade uncertainty, and U.K. demand remains subdued in line with weaker economic activity.

Across Asia, performance is mixed: Australia continues to outperform with structurally low vacancy (3–4%) and demand driven by population growth and eCommerce, while Japan faces elevated vacancies due to excess supply.

Looking ahead, industrial performance will likely diverge further, with leading markets tied to technological, manufacturing and defense ecosystems, cost efficiency, and locations with higher disposable incomes and retail sales growth. Outperforming assets are expected to be concentrated in power-ready logistics facilities critical for automation and fleet charging.

Residential

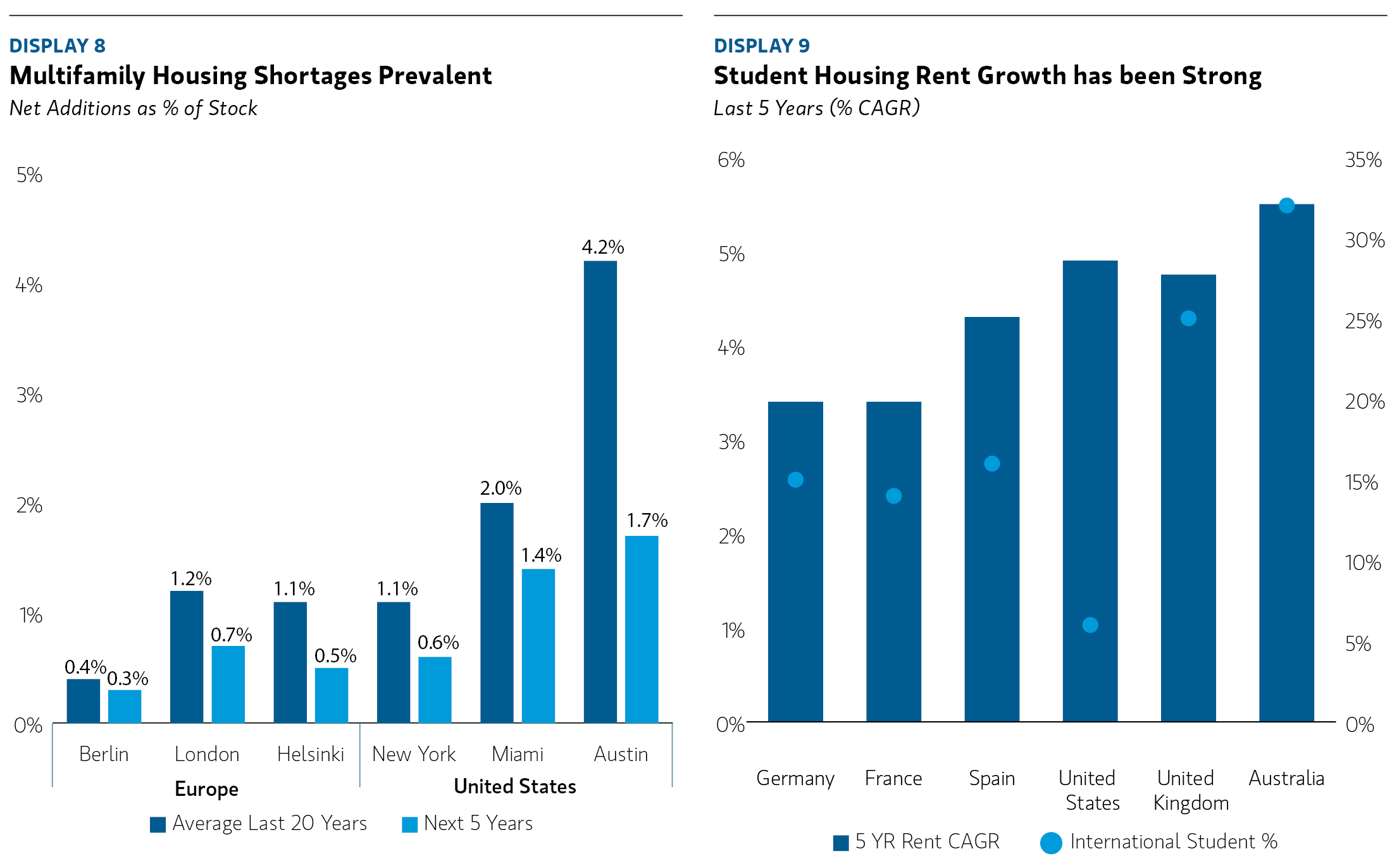

The for-rent residential sector remains supported by long-term structural trends, including constrained for-sale affordability and persistent supply shortages. Performance drivers vary globally: in the U.S., outcomes hinge on migration trends, aging demographics, regulatory pressures, and the speed of the supply response. In Europe, rental growth is fueled by urbanization and severe supply gaps, with housing deliveries falling far short of government targets (e.g., 150,000 vs. 300,000 in the U.K.; 200,000 vs. 400,000 in Germany)8. In Japan, high single-digit rent growth reflects steady demographic inflows—including foreign nationals—urbanization, wage gains, and elevated condo prices, reinforcing renter demand.

Global housing dynamics are shifting from a supply-driven narrative to demand-led trends as job growth moderates, immigration slows, and migration patterns normalize—creating new market winners and losers. In the U.S., domestic out-migration from gateway to sunbelt markets is slowing, with modest population gains in New York (+0.1%), Chicago (+0.2%), and San Francisco (+0.1%) over the past 12 months9, compared to prior declines. In Japan, despite nationwide population contraction, Tokyo’s inner wards continue grow, due to foreign and rural inflows which added over 80,000 residents through August 202510. In Europe, slowing immigration has been offset by urbanization and household decoupling, sustaining positive household formation.

As an extension to traditional residential opportunities, student housing remains attractive, particularly for high-quality, well-located assets near leading universities, supported by resilient enrollment, moderating supply, and strong yield profiles. For example, in the U.S., enrollment at Power 5 universities has grown by 9% since 201911, versus declining for other types of universities. The potential slowdown in foreign students and federal research grants will continue to challenge some universities, requiring a selective investment approach. In Europe, the growth of domestic and international students (particularly in markets like Spain) combined with low supply of purpose-built student housing assets should lead to continued outsized rent growth in the near-term.

While residential real estate offers compelling fundamentals in most markets and sub-segments due to a positive demand/supply imbalance, regulatory risks remain elevated, and the capital markets remain very competitive fueled by accretive and liquid debt markets.

Office

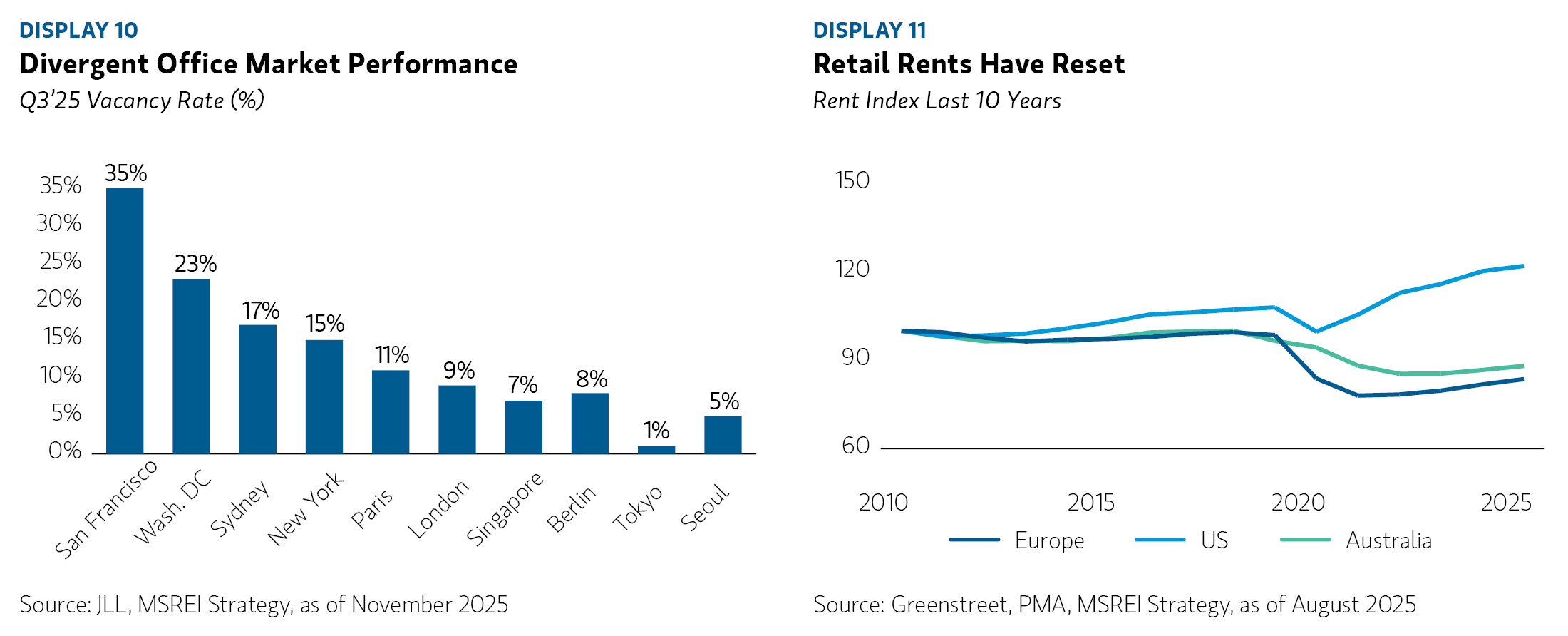

While global office markets like Tokyo, Seoul, Paris, and London have performed well over the past several years, only recently have select U.S. markets seen stronger fundamentals and improved investor sentiment, with return-to-office and occupier uncertainty largely behind us. Class A assets are achieving record rents as demand consolidates around high-quality, amenitized, well-located properties—driving renewed investor interest across equity and debt. However, significant capital expenditures for leasing and maintenance (particularly in the U.S. and Australia), ESG requirements, cyclical job moderation, and concerns over AI’s long-term impact on office employment continue to pose performance headwinds.

Retail

The retail sector remains resilient, supported by strong sales growth and reduced supply in key markets, including the United States. Lower rents have eased occupancy costs, while yields have widened. Performance varies by segment: grocery-anchored centers show the greatest stability, and luxury-focused shopping centers have also outperformed, driven by the financial strength of high-income consumers. Markets with robust employment and dense populations continue to lead. Overall, limited quality supply and minimal new development are expected to sustain occupancy and drive future rent growth.

Hospitality

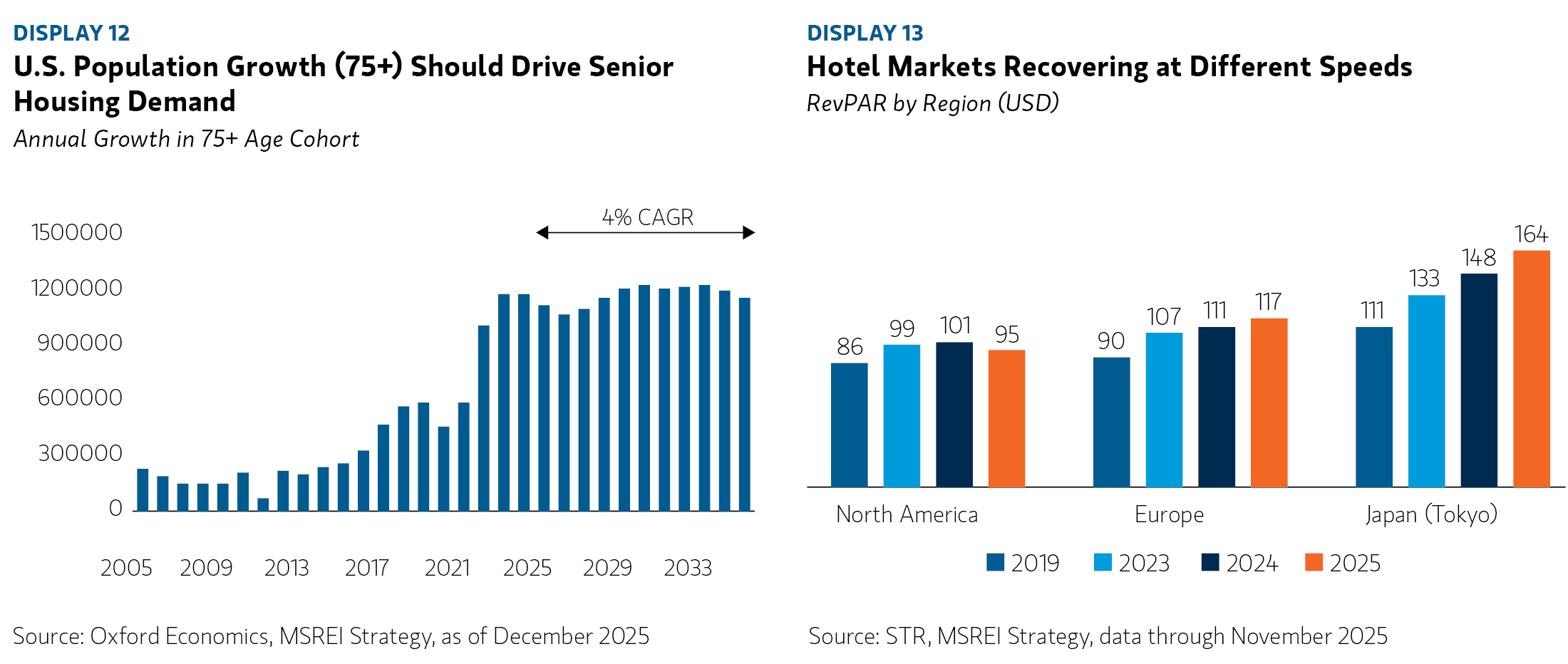

Long-term trends remain largely favorable for hotels, with the decline in business travel offset by demographic shifts as millennials — the largest age cohort in many countries — prioritize travel and experiences over goods. Preferred assets are those with diversified demand drivers beyond business or leisure and located in supply-constrained urban markets rather than resorts. Markets such as Japan and Europe benefit from international tourism rather than relying solely on domestic growth or local GDP.

Healthcare

Fundamentals vary across healthcare subsectors; with senior housing remaining strong, medical office solid, and life science still very challenged. Senior housing offers compelling risk-adjusted returns, driven by strong demographic tailwinds and limited supply. The U.S. 75+ population is projected to grow 4–5% annually over the next five years, creating sustained demand12. This sector combines high yields with growth potential, providing downside protection through cash flow and upside from long-term trends. Unlike other residential segments, senior housing benefits from improving affordability as baby boomers leverage wealth from home and equity appreciation. While aging demographics are a global theme, the U.S. remains the most attractive investment market due to its institutional scale, supportive cultural norms, and favorable regulatory environment.

The life science segment faces headwinds from both weak demand and oversupply. Institutional appetite for lab space has declined due to reduced activity from early-stage venture-backed firms, larger public biotech companies, and government funding. Meanwhile, speculative development, including suburban office conversions, has created a significant supply-demand imbalance.

Medical office fundamentals remain strong, with outpatient care demand projected to grow 11% versus less than 1% for inpatient over the next five years13. This shift is driven by technology enabling more outpatient procedures and a focus on chronic care management. Demand has grown 3.7% annually since 2000, closely tied to healthcare spending, which rose 5.6% annually and is expected to grow 5.8% over the next decade14 —supporting continued robust demand, especially for higher-acuity services.

Self-Storage

Elevated mortgage rates, sluggish existing home sales and overall concerns over affordability have slowed storage demand. However pent-up home buying demand and lower supply should lead to improved fundamentals over the medium term.

Net Lease

Net lease investments in sectors and assets that are generally less sensitive to the cyclical economy are expected to perform well given their durable, long-term cashflows with fixed escalations. These investments are particularly attractive today given they are less exposed to risks associated with both slowing economic growth (exposure to rent volatility) and rising inflation (as the investor is not responsible for increases in taxes, wages, capital expenditures or insurance costs). However, to be successful, investors need to balance tenant credit quality with the underlying quality of the real estate. Return outperformance is ultimately underpinned by renewal probability, which is directly shaped by the mission criticality of the underlying real estate assets.

Data Centers

Data center fundamentals remain strong, driven by robust hyperscaler leasing and limited supply due to power constraints. While the U.S. is the primary market, global tech firms are expanding rapidly in Europe and Asia-Pacific, fueling demand. These dynamics attract deep capital pools, creating a highly competitive environment with tight pricing despite AI-bubble concerns. Indirect opportunities exist in traditional sectors—such as industrial and residential—in locations benefiting from AI and data center growth.

Conclusion

After two years of declining values and a further two years of stagnation, MSREI expects 2026 to mark an inflection point for increased transaction activity and value growth. Lower interest rates, reduced macroeconomic risks, and constrained supply create favorable conditions for recovery, though performance will vary across regions, sectors, and asset types. This environment requires granular, market-specific, plus asset-level strategies and an intense focus on asset management to generate meaningful NOI growth.

Analyses mises en avant