An investor cannot focus on growth and avoid obsolescence at the same time—innovation doesn’t work that way. The investor’s job is not to hide from AI disruption, but to manage it and monetize the potential dispersion it creates.

One of the most frequently asked questions I get is: How are we managing the uncertainty and volatility surrounding AI disruption, particularly when the narrative often takes on a doomsday tone?

The short answer is that risks in today’s market are largely idiosyncratic. But, with diversification, balance sheet discipline and sound portfolio construction, volatility can be mitigated and often transformed into opportunity. To understand why, it is helpful to revisit the idea of HALO—Heavy Assets, Low Obsolescence—and look at it in a broader investment context. HALO is a conceptual framework designed to mitigate the risk of the disruption spawned by AI that may sow volatility across markets.

The concept of Heavy Assets has intuitive appeal. Real assets, infrastructure, commodities and certain industrial platforms tend to provide resilience. They are capital intensive, difficult to replicate and often benefit from embedded scarcity value. History reinforces this. Energy and real assets outperformed during the inflationary 1970s. Infrastructure and hard assets repriced positively during post-COVID supply constraints, when scarcity once again became economically relevant. Hard assets matter, particularly when inflation or supply friction reemerges.

The idea of Low Obsolescence, however, is more complicated. Low obsolescence runs counter to innovation, productivity gains and technological progress. Markets evolve and creative destruction is not a flaw in capitalism. On the contrary, it is a defining feature. Railroads were once considered permanent monopolies, yet trucking and aviation reshaped transportation economics. Kodak possessed brand power and distribution dominance, but technological change rendered its business model obsolete. True “low obsolescence plus high growth” assets are rare. Obsolescence cannot be avoided; in fact, it must be actively managed.

This reveals a core tension in investing. There is a structural conflict between high growth, which can generate high returns, and low obsolescence stability, which may generate subpar returns. Innovation increases growth potential, but also raises the probability of disruption. As investors, we embrace productivity gains while actively managing obsolescence risk. In our approach, it is critical to avoid confusing durability with permanence.

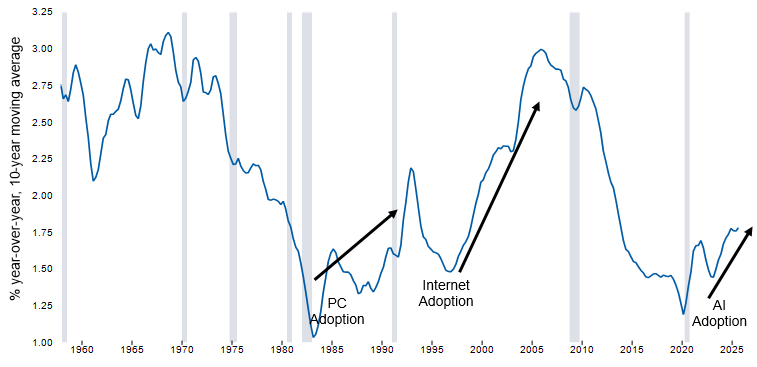

Display 1

Productivity Growth Appears To Be Rising Again

Display 1

Productivity Growth Appears To Be Rising Again

Nonfarm business labor productivity: output per hour

AI represents creative destruction in real time. It is not cyclical; it is structural. AI will disrupt labor models, cost structures, pricing power and capital allocation. It will reprice assets whose economics depend on scarcity of knowledge, process or distribution. The key investment question is not whether AI will cause disruption. It most certainly will. What needs to be determined is whether disruption intersects with leverage in a way that creates systemic contagion—or whether it remains dispersed across sectors and business models. This is a key distinction of great importance.

Contagion occurs when disruption meets high leverage. The result can be forced deleveraging, rising cross-asset correlations and credit stress. The 2008 global financial crisis is the clearest example: housing disruption combined with excessive leverage produced systemic consequences.

Dispersion, by contrast, occurs when disruption is contained in specific sectors, credit markets remain stable and the broader macroeconomic backdrop holds. The 2000–2002 dotcom unwind produced severe equity dispersion, but limited credit stress. The transition to the cloud and software of the 2010s compressed legacy technology valuations while new platforms compounded.

Today’s environment more closely resembles dispersion than contagion. Stress is concentrated. Credit markets are not signaling systemic instability. Employment, earnings and inflation remain broadly constructive. Dispersion, importantly, expands the opportunity set.

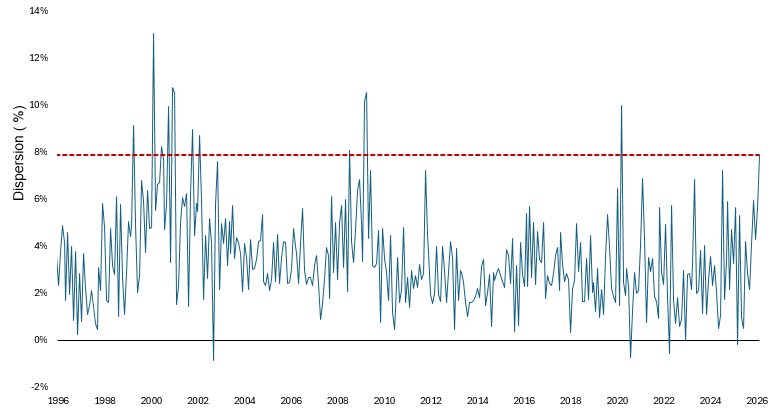

Display 2

Higher Dispersion Creates Opportunity for Active Management

Display 2

Higher Dispersion Creates Opportunity for Active Management

S&P 500 constituent average 30-day move less S&P 500 absolute move, 30-year lookback

This is precisely the type of environment that favors active management. AI-driven volatility creates valuation gaps. It widens dispersion across sectors and factors. It punishes incumbents while rewarding productivity beneficiaries. Passive strategies, by design, must own both the disruptors and the disrupted. Active strategies have a choice and can stress-test balance sheets, avoid highly-levered business models vulnerable to automation and reallocate capital toward companies positioned to harness productivity gains. Historically, periods of elevated dispersion—such as the early 2000s or the post-global financial crisis technology cycle—rewarded selective positioning.

AI also creates identifiable areas of valuation risk. Business models reliant on information scarcity are vulnerable. Labor-heavy cost structures with limited pricing power face margin compression. Companies with high fixed costs, high leverage and low switching costs are particularly exposed. Valuations adjust most rapidly when optimistic growth assumptions collide with structural margin pressure, especially when disruption meets leverage.

At the same time AI represents a positive productivity shock. Beneficiaries are likely to include scalable platform businesses, asset-light models leveraging data and network effects, and hard asset owners integrating AI to expand margins. Infrastructure enabling computation, energy and connectivity stands to benefit from rising demand. History provides useful parallels. In the early twentieth century electrification disrupted some industries while transforming many others. The internet destroyed traditional media economics but created entirely new ecosystems. Creative destruction reallocates capital; it does not eliminate it.

From a multi-asset perspective, several implications follow. In equities, we should expect wider dispersion and place greater emphasis on balance sheet strength and pricing power, while avoiding highly-levered legacy models vulnerable to automation. In credit, monitoring the intersection of leverage and technological vulnerability is critical. As long as dispersion remains contained and correlations stable, credit markets can remain resilient. Signs of contagion would include rising cross-asset correlations and funding stress. With respect to real assets, hard assets retain relevance in inflationary regimes, and AI-driven demand for power, data centers and connectivity infrastructure provides structural support.

In portfolio construction, it is essential to incorporate diversification across the beneficiaries of disruption and durable asset classes. Correlations should be stress-tested under leverage shock scenarios, and volatility should be embraced when it reflects dispersion rather than systemic instability.

The bottom line is straightforward. AI is creative destruction unfolding in real time. The risk is not disruption alone; it’s the risk of disruption combined with leverage. Today’s environment appears more characterized by dispersion than contagion. Dispersion creates pricing gaps, and pricing gaps create opportunity.

Our role is not to predict every winner in the AI arena. Our responsibility is to manage obsolescence, rigorously stress-test leverage, exploit dispersion and allocate capital where productivity gains can compound over time. This creates thematic investment opportunities that are incorporated into the strategies we manage.

Creative destruction will always generate headlines. Disciplined active management, executed consistently and grounded in valuation and balance sheet analysis, is what converts structural change into long-term returns.

Featured Insights