A sharp reversal from 2025 and a compelling setup for what's next

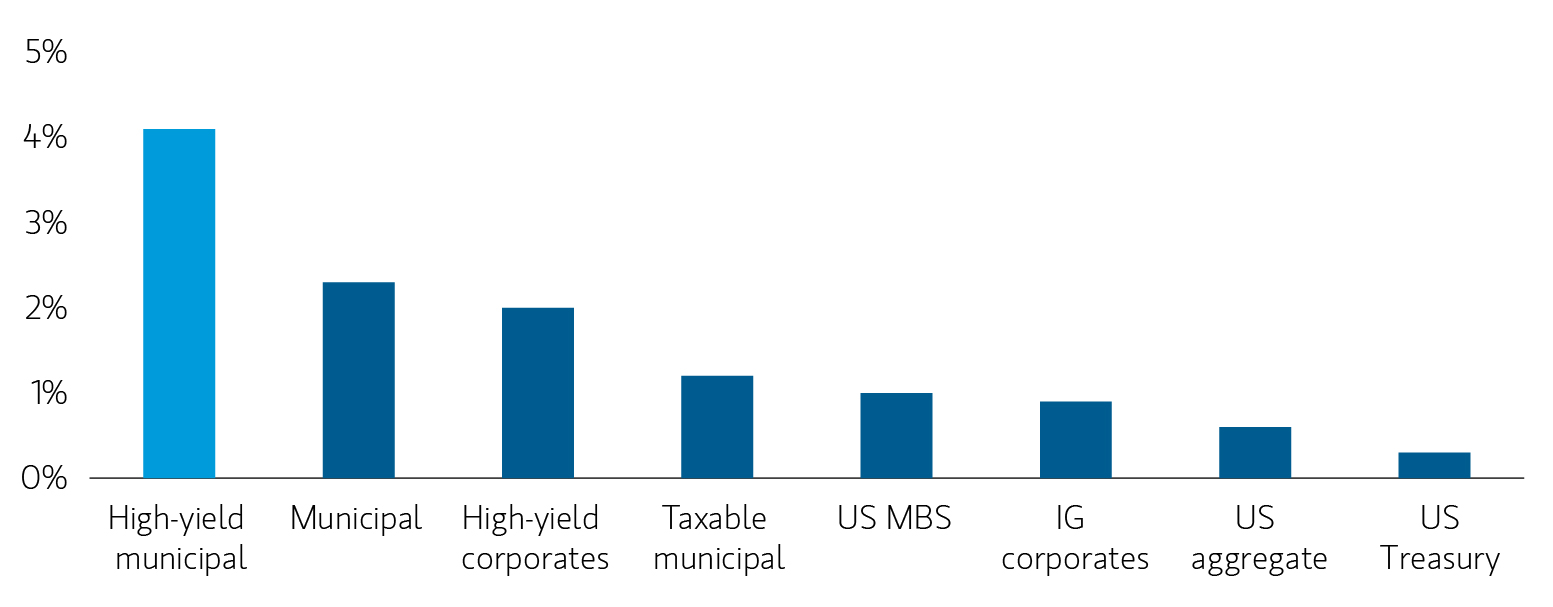

After a challenging 2025, in which high-yield municipals underperformed their investment-grade (IG) counterparts, the narrative has shifted decisively in 2026. Year-to-date (YTD), high-yield munis are not only outperforming IG munis, they’re outperforming virtually every other major fixed income asset class. We believe this outperformance is likely to continue, supported by three reinforcing tailwinds: elevated yields, favorable supply-demand technicals and solid credit fundamentals.

For investors who looked past last year's volatility, we believe the current setup offers one of the more attractive risk-adjusted opportunities in fixed income today.

Year-to-date sector performance

Source: Bloomberg Indexes as of June 30, 2026. See indices used to represent the categories and the Index definitions in the disclosure section at the back. For illustrative purposes only. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index. Past performance is not indicative of future results. Treasury bills and bonds are backed by the full faith and credit of the US government if held to maturity. Fixed income securities are subject to the ability of an issuer to make timely principal and interest payments (credit risk), changes in interest rates (interest-rate risk), the creditworthiness of the issuer and general market liquidity (market risk). High yield securities (“junk bonds”) are lower rated securities that may have a higher degree of credit and liquidity risk. See Risk Considerations below for more information.

Year-to-date sector performance

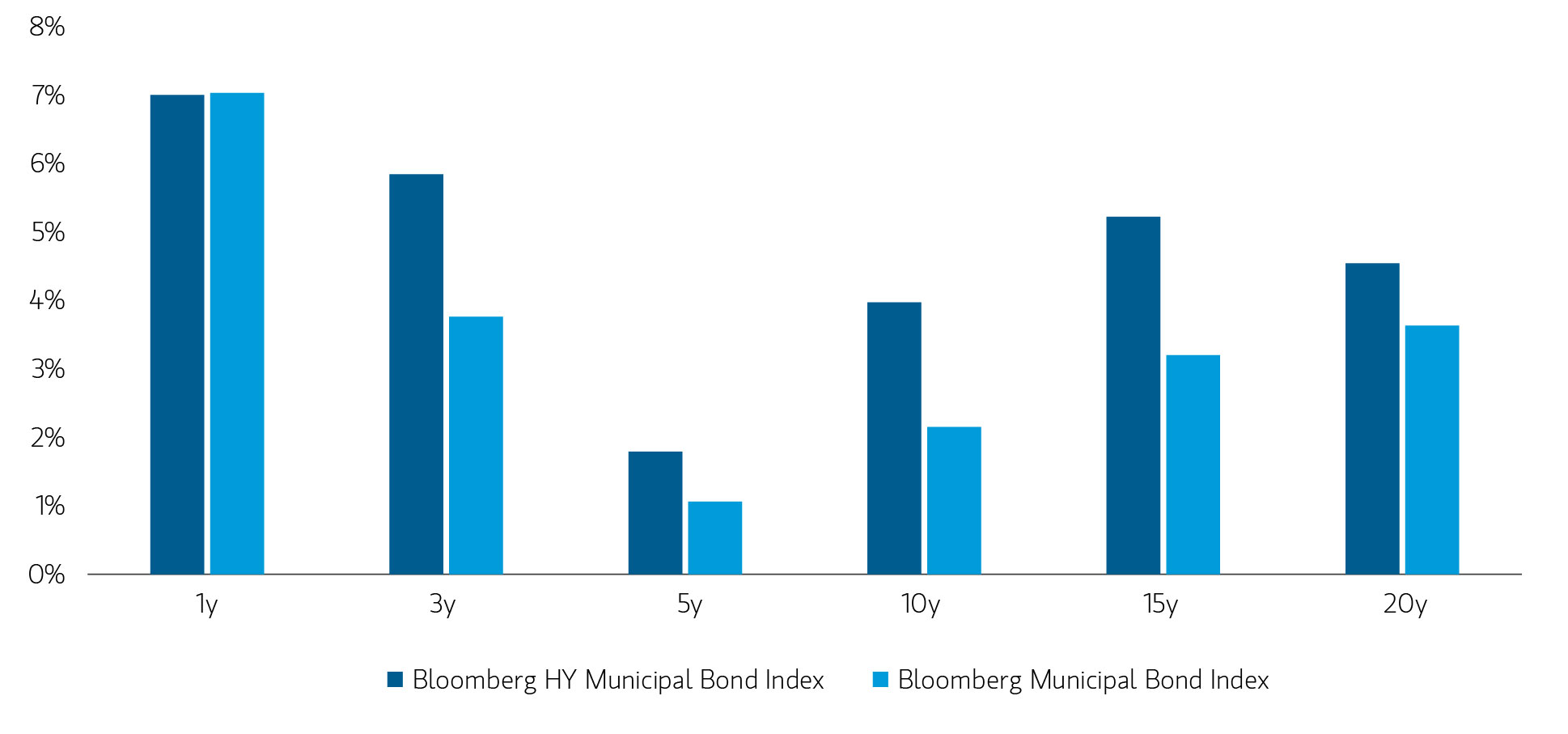

Strong long-term performance

History has shown that high-yield munis have consistently outperformed IG munis over longer investment horizons. Much of this outperformance has been driven by higher coupon income, which has historically helped offset periods of rising interest rates and market volatility.

Unlike traditional IG muni bonds, where interest rate movements often dominate returns, high-yield munis are more heavily influenced by issuer-specific credit fundamentals since they have a higher degree of credit and liquidity risk than IG muni bonds. As a result, the additional income generated by the sector has historically produced superior long-term total returns despite occasional periods of short-term underperformance.

High-yield municipals have delivered higher long-term returns

Source: Bloomberg Indexes as of June 30, 2026. High Yield is represented by the Bloomberg High Yield Municipal Bond Index; Municipal is represented by the Bloomberg Municipal Bond Index. For illustrative purposes only. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index. Past performance is not indicative of future results.

High-yield municipals have delivered higher long-term returns

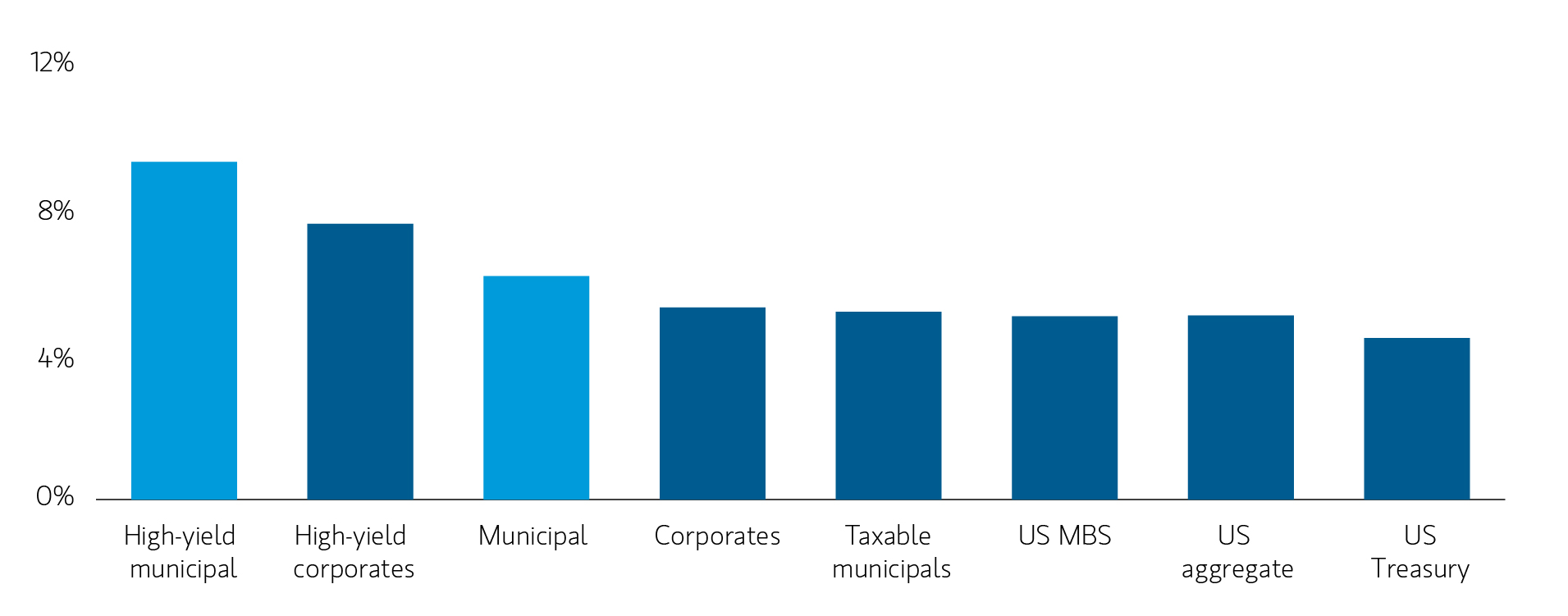

Elevated yields provide a powerful starting point

Income remains the single most important driver of long-term muni returns, and today's starting yields are among the most attractive in over a decade. Current tax-equivalent yields on high-yield munis compare favorably with, and in many cases exceed, yields available across taxable fixed income sectors, including high-yield corporates, IG corporates, MBS, and Treasurys.

Municipal taxable-equivalent yields remain attractive relative to other fixed income alternatives

Source: Bloomberg Indexes as of June 30, 2026. Taxable-equivalent yield is calculated assuming a federal tax rate of 40.80% -- details and index definitions below. High Yield is represented by the Bloomberg High Yield Municipal Bond Index; High Yield Corporate is represented by the Bloomberg U.S. Corporate High Yield Index; Municipal is represented by the Bloomberg Municipal Bond Index; Taxable Municipal is represented by the Bloomberg Taxable Municipal Bond Index; Corporate is represented by the Bloomberg U.S. Corporate Investment Grade Index; U.S. MBS is represented by the Bloomberg U.S. Mortgage-Backed Securities (MBS) Index; U.S. Aggregate stands for the Bloomberg U.S. Aggregate Index; U.S. Treasury is represented by the Bloomberg U.S. Treasury Index. For illustrative purposes only. Not a recommendation to buy or sell any security. It is not possible to invest directly in an index. Past performance is not indicative of future results.

Municipal taxable-equivalent yields remain attractive relative to other fixed income alternatives

For investors in higher tax brackets, the after-tax math is especially compelling: High-yield munis can deliver meaningful incremental income without sacrificing the tax advantages that have long anchored muni allocations.

Technicals: Reduced issuance meets solid demand

Technical conditions in the high-yield muni market remain decidedly supportive.

On the supply side, while overall muni issuance hit a record in 2025 and is on pace for another record in 2026, high-yield muni issuance has remained notably constrained — representing only a small fraction of total new-issue volume. From 2019 to 2025 high-yield muni issuance averaged over 8% of total muni issuance. However, year-to-date through June 2026, high-yield muni issuance totaled just $16 billion, or 6% of total issuance.

On the demand side, fund flows have remained healthy, supported by high-income investors seeking attractive after-tax yields and renewed interest from institutional buyers.

This combination—limited new supply meeting steady, broad-based demand—has historically provided a powerful technical tailwind for the asset class, and we expect it to remain a key driver of relative performance through the balance of 2026.

Credit fundamentals remain solid

The broader muni credit backdrop continues to support the asset class. State and local governments generally maintain healthy reserve balances, tax collections have remained resilient and rating agencies continue to report more upgrades than downgrades across much of the muni market.

Default rates for muni bonds remain well below those of similarly rated corporate bonds, and recovery rates have historically been significantly higher. Much of this resilience stems from the nature of muni issuers themselves. Many high-yield credits finance essential community infrastructure such as hospitals, charter schools, transportation systems, utilities and senior housing, often secured by dedicated revenue streams or project-specific collateral.

Make no mistake: This is an idiosyncratic asset class

While the macro setup is compelling, high-yield munis are fundamentally a credit-driven, idiosyncratic asset class and high-yield muni returns are dominated by issuer-specific credit outcomes. This underscores why active, deep, bottom-up credit analysis is essential.

This year has provided clear reminders of that dynamic. Weakness in a regional high-speed train company and certain New York tobacco bonds has highlighted how individual credit stories can deviate sharply from the broader asset class. These aren’t systemic concerns; they’re issuer-specific challenges that disciplined credit research can identify and avoid.

In an asset class where a handful of problem credits can drive a disproportionate share of underperformance, identifying and sidestepping those names is as important as identifying the winners.

A complement to traditional municipal allocations

For many investors, the question isn’t whether to own IG munis or high-yield munis; it’s whether a thoughtful combination can produce a more efficient portfolio.

IG munis continue to provide relative stability and high credit quality. High-yield munis, meanwhile, can complement that allocation by enhancing portfolio income, improving long-term return potential, and increasing tax-free cash flow, albeit with greater credit and liquidity risk. Given the sector's complexity, fragmented issuer base and significant proportion of unrated securities, active credit research remains the single most important factor in capturing the opportunity while managing the risk.

The bottom line

After lagging IG munis in 2025, high-yield munis have reasserted themselves in 2026, leading not just the muni market but virtually all fixed income year-to-date. With elevated yields, supportive supply-demand technicals and solid underlying credit fundamentals, we believe the conditions for continued outperformance remain firmly in place.

Featured Insights

Index definitions

Bloomberg High Yield Municipal Bond Index is an unmanaged index of non-Investment Grade Municipal bonds traded in the U.S.

Bloomberg U.S. Corporate High Yield Index is an unmanaged index consisting of domestic and corporate bonds rated Ba and below with a minimum outstanding amount of $150 million. You cannot invest directly in an index.

Bloomberg Municipal Bond Index is an unmanaged index of Municipal bonds traded in the U.S.

Bloomberg Taxable Municipal Bond Index is an unmanaged index of Taxable Municipal bonds traded in the U.S.

Bloomberg U.S. Corporate Investment Grade Index is an unmanaged index that measures the performance of investment-grade corporate securities within the Barclays U.S. Aggregate Index.

Bloomberg U.S. Aggregate Index is an unmanaged index of domestic investment-grade bonds, including corporate, government and mortgage-backed securities.

Bloomberg U.S. Mortgage-Backed Securities (MBS) Index measures agency mortgage-backed pass-through securities issued by GNMA, FNMA, and FHLMC.

Bloomberg U.S. Treasury Index measures public debt instruments issued by the U.S. Treasury, excluding short-term Treasury bills.

High Yield is represented by the Bloomberg High Yield Municipal Bond Index; High Yield Corporate is represented by the Bloomberg U.S. Corporate High Yield Index; Municipal is represented by the Bloomberg Municipal Bond Index; Taxable Municipal is represented by the Bloomberg Taxable Municipal Bond Index; Corporate is represented by the Bloomberg U.S. Corporate Investment Grade Index; U.S. MBS is represented by the Bloomberg U.S. Mortgage-Backed Securities (MBS) Index; U.S. Aggregate stands for the Bloomberg U.S. Aggregate Index; U.S. Treasury is represented by the Bloomberg U.S. Treasury Index.

Risk Considerations: There is no assurance that a portfolio will achieve its investment objective. Portfolios are subject to market risk, which is the possibility that the market values of securities owned by the portfolio will decline and that the value of portfolio shares may therefore be less than what you paid for them. Market values can change daily due to economic and other events (e.g., natural disasters, health crises, terrorism, conflicts, and social unrest) that affect markets, countries, companies or governments. It is difficult to predict the timing, duration, and potential adverse effects (e.g., portfolio liquidity) of events. Accordingly, you can lose money investing in a portfolio. Fixed-income securities are subject to the ability of an issuer to make timely principal and interest payments (credit risk), changes in interest rates (interest rate risk), the creditworthiness of the issuer and general market liquidity (market risk). In a rising interest-rate environment, bond prices may fall and may result in periods of volatility and increased portfolio redemptions. In a declining interest-rate environment, the portfolio may generate less income. Longer-term securities may be more sensitive to interest rate changes. High yield securities (“junk bonds”) are lower rated securities that may have a higher degree of credit and liquidity risk. An imbalance in supply and demand in the municipal market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. There generally is limited public information about municipal issuers. Income from tax-exempt municipal obligations could be declared taxable because of changes in tax laws, adverse interpretations by the relevant taxing authority or the non-compliant conduct of the issuer of an obligation and may be subject to the federal alternative minimum tax.

There is no guarantee that any investment strategy will work under all market conditions, and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market.

A separately managed account may not be appropriate for all investors. Separate accounts managed according to the particular strategy may include securities that may not necessarily track the performance of a particular index. Please consider the investment objectives, risks and fees of the Strategy carefully before investing. A minimum asset level is required. For important information about the investment managers, please refer to Form ADV Part 2.

The views and opinions and/or analysis expressed are those of the author or the investment team as of the date of preparation of this material and are subject to change at any time without notice due to market or economic conditions and may not necessarily come to pass. Furthermore, the views will not be updated or otherwise revised to reflect information that subsequently becomes available or circumstances existing, or changes occurring, after the date of publication. The views expressed do not reflect the opinions of all investment personnel at Morgan Stanley Investment Management (MSIM) and its subsidiaries and affiliates (collectively “the Firm”) and may not be reflected in all the strategies and products that the Firm offers.

Forecasts and/or estimates provided herein are subject to change and may not actually come to pass. Information regarding expected market returns and market outlooks is based on the research, analysis and opinions of the authors or the investment team. These conclusions are speculative in nature, may not come to pass and are not intended to predict the future performance of any specific strategy or product the Firm offers. Future results may differ significantly depending on factors such as changes in securities or financial markets or general economic conditions.

This material has been prepared on the basis of publicly available information, internally developed data and other third-party sources believed to be reliable. However, no assurances are provided regarding the reliability of such information and the Firm has not sought to independently verify information taken from public and third-party sources.

This material is a general communication, which is not impartial, and all information provided has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy. The information herein has not been based on a consideration of any individual investor circumstances and is not investment advice, nor should it be construed in any way as tax, accounting, legal or regulatory advice. To that end, investors should seek independent legal and financial advice, including advice as to tax consequences, before making any investment decision.

The Firm does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. It was not intended or written to be used, and it cannot be used by any taxpayer, for the purpose of avoiding penalties that may be imposed on the taxpayer. Each Jurisdiction’s tax laws are complex and constantly changing. You should always consult your own legal or tax professional for information concerning your individual situation.

Charts and graphs provided herein are for illustrative purposes only. Past performance is no guarantee of future results.

The indexes are unmanaged and do not include any expenses, fees or sales charges. It is not possible to invest directly in an index. Any index referred to herein is the intellectual property (including registered trademarks) of the applicable licensor. Any product based on an index is in no way sponsored, endorsed, sold or promoted by the applicable licensor and it shall not have any liability with respect thereto.

This material is not a product of Morgan Stanley’s Research Department and should not be regarded as a research material or a recommendation.

The Firm has not authorized financial intermediaries to use and to distribute this material, unless such use and distribution is made in accordance with applicable law and regulation. Additionally, financial intermediaries are required to satisfy themselves that the information in this material is appropriate for any person to whom they provide this material in view of that person’s circumstances and purpose. The Firm shall not be liable for, and accepts no liability for, the use or misuse of this material by any such financial intermediary.

This material may be translated into other languages. Where such a translation is made this English version remains definitive. If there are any discrepancies between the English version and any version of this material in another language, the English version shall prevail.

The whole or any part of this material may not be directly or indirectly reproduced, copied, modified, used to create a derivative work, performed, displayed, published, posted, licensed, framed, distributed or transmitted or any of its contents disclosed to third parties without the Firm’s express written consent. This material may not be linked to unless such hyperlink is for personal and non-commercial use. All information contained herein is proprietary and is protected under copyright and other applicable law.

Eaton Vance, Atlanta Capital, Parametric and Calvert are part of Morgan Stanley Investment Management. Morgan Stanley Investment Management is the asset management division of Morgan Stanley.

DISTRIBUTION

This material is only intended for and will only be distributed to persons resident in jurisdictions where such distribution or availability would not be contrary to local laws or regulations.

MSIM, the asset management division of Morgan Stanley (NYSE: MS), and its affiliates have arrangements in place to market each other’s products and services. Each MSIM affiliate is regulated as appropriate in the jurisdiction it operates. MSIM’s affiliates are: Calvert Research and Management, Eaton Vance Management, Parametric Portfolio Associates LLC, Parametric SAS, and Atlanta Capital Management LLC.

This material has been issued by any one or more of the following entities:

EMEA

This material is for Professional Clients/Accredited Investors only.

In the EU, MSIM materials are issued by MSIM Fund Management (Ireland) Limited (“FMIL”). FMIL is regulated by the Central Bank of Ireland and is incorporated in Ireland as a private company limited by shares with company registration number 616661 and has its registered address at 24-26 City Quay, Dublin 2, DO2 NY19, Ireland.

Outside the EU, MSIM materials are issued by Morgan Stanley Investment Management Limited (MSIM Ltd) is authorised and regulated by the Financial Conduct Authority. Registered in England. Registered No. 1981121. Registered Office: 25 Cabot Square, Canary Wharf, London E14 4QA.

In Switzerland, MSIM materials are issued by Morgan Stanley & Co. International plc, London (Zurich Branch) Authorised and regulated by the Eidgenössische Finanzmarktaufsicht ("FINMA"). Registered Office: Beethovenstrasse 33, 8002 Zurich, Switzerland.

Italy: MSIM FMIL (Milan Branch), (Sede Secondaria di Milano) Palazzo Serbelloni Corso Venezia, 16 20121 Milano, Italy. The Netherlands: MSIM FMIL (Amsterdam Branch), Rembrandt Tower, 11th Floor Amstelplein 1 1096HA, Netherlands. France: MSIM FMIL (Paris Branch), 61 rue de Monceau 75008 Paris, France. Spain: MSIM FMIL (Madrid Branch), Calle Serrano 55, 28006, Madrid, Spain. Germany: MSIM FMIL Frankfurt Branch, Große Gallusstraße 18, 60312 Frankfurt am Main, Germany (Gattung: Zweigniederlassung (FDI) gem. § 53b KWG). Denmark: MSIM FMIL (Copenhagen Branch), Gorrissen Federspiel, Axel Towers, Axeltorv2, 1609 Copenhagen V, Denmark.

MIDDLE EAST

Dubai International Financial Centre: This information does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe for or purchase, any securities or investment products in the UAE (including the Dubai International Financial Centre and the Abu Dhabi Global Market) and accordingly should not be construed as such. Furthermore, this information is being made available on the basis that the recipient acknowledges and understands that the entities and securities to which it may relate have not been approved, licensed by or registered with the UAE Central Bank, the Dubai Financial Services Authority, the UAE Securities and Commodities Authority, the Financial Services Regulatory Authority or any other relevant licensing authority or government agency in the UAE. The content of this report has not been approved by or filed with the UAE Central Bank, the Dubai Financial Services Authority, the UAE Securities and Commodities Authority or the Financial Services Regulatory Authority.

Abu Dhabi Global Market ("ADGM"): This material is sent strictly within the context of, and constitutes, an Exempt Communication. This material relates to (strategy) which is not subject to any form of regulation or approval by the Financial Services Regulatory Authority of the Abu Dhabi Global Market (the “FSRA”).

Saudi Arabia

This financial promotion was issued and approved for use in Saudi Arabia by Morgan Stanley Saudi Arabia, Al Rashid Tower, Kings Sand Street, Riyadh, Saudi Arabia, authorized and regulated by the Capital Market Authority license number 06044-37.

U.S.

NOT FDIC INSURED | OFFER NO BANK GUARANTEE | MAY LOSE VALUE | NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY | NOT A DEPOSIT

Latin America (Brazil, Chile Colombia, Mexico, Peru, and Uruguay)

This material is for use with an institutional investor or a qualified investor only. All information contained herein is confidential and is for the exclusive use and review of the intended addressee, and may not be passed on to any third party. This material is provided for informational purposes only and does not constitute a public offering, solicitation or recommendation to buy or sell for any product, service, security and/or strategy. A decision to invest should only be made after reading the strategy documentation and conducting in-depth and independent due diligence.