Macro versus Micro

- “I don’t understand why the stock market is at an all-time-high” is a consistent refrain I hear lately from many investors.

My first thought is, “that’s because you are overly focused on the macro.”

Confusion is certainly legitimate, given the scary headlines of late.

Whether it is about the potential for the Iran War to cause an inflation spike, for Ai innovation to result in a wave of layoffs or even for private credit problems to lead to the next financial crisis…

There is plenty to worry about. - Yet what is currently happening at the micro level is a very powerful story.

Apologies as I don my professorial cap to remind everyone that stocks are the present value of future business expectations.

The direction of change in the interpretation of future fundamentals primarily determines a stock's price movement.

Collectively, if Wall Street raises expectations about a company’s future, its stock should respond positively.

Likewise, when a company alerts Wall Street their business is not as good as anticipated, down goes the stock.

Since the stock market is comprised of an index of stocks, cumulative changes in future expectations affect the stock market overall. - Companies are signaling their fundamentals are currently MUCH better than what was expected.

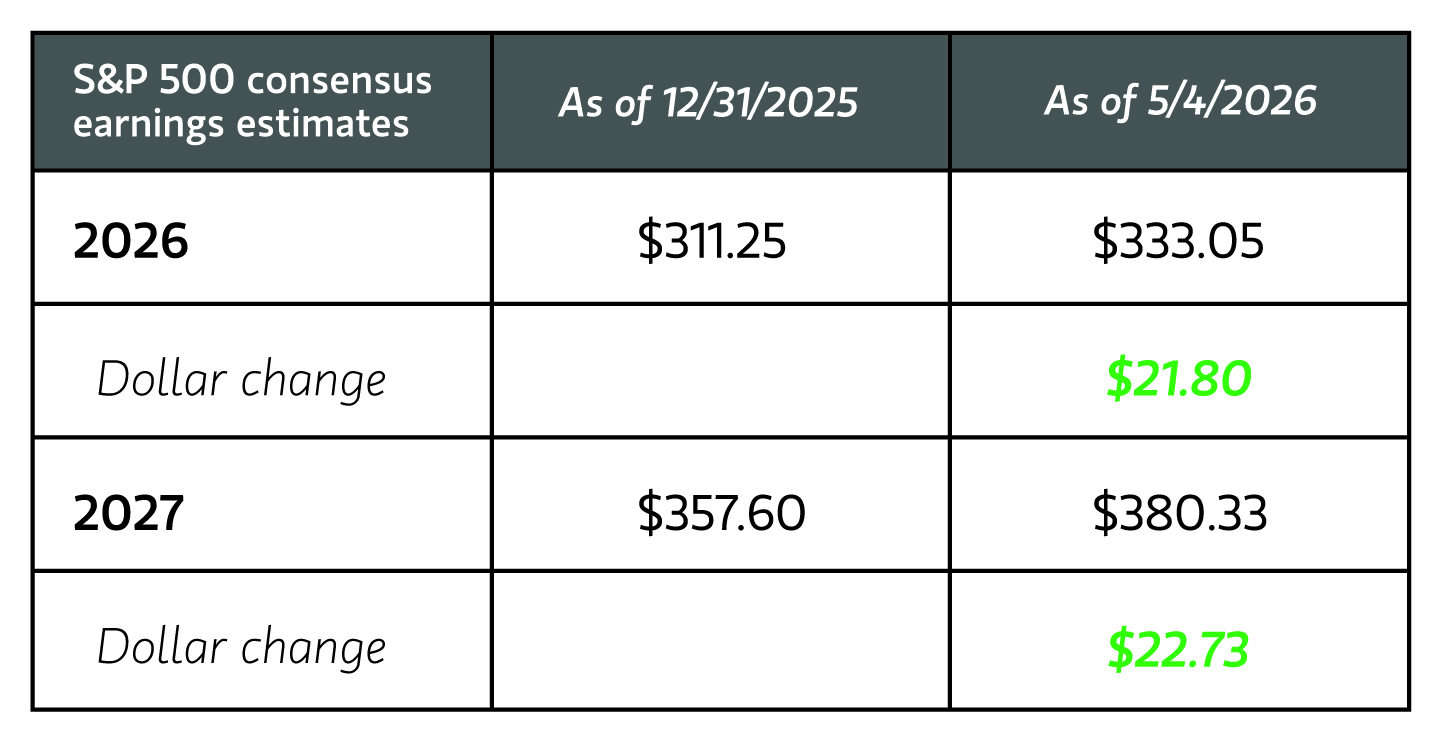

Here are the Factset 2026 and 2027 bottom-up earnings estimates for the S&P 500 as of May 4th, versus where they started the year.

×

I have worked in the investing world for a long time and have never seen this magnitude of increases.

These incredibly positive revisions are extremely bullish.

- Of the two years, the 2027 estimate is the more important number.

As an investor, if one thinks about where the S&P 500 could end the year on December 31st, 2026, the next 12 months earnings will be for 2027.

That number is already up $22.73, and it’s only early May 2026!

- Unfortunately, the business headlines overplay the macro and underplay the micro, in my opinion.

While political biases can be a cause, I think macro headlines are more likely to capture readers’ attention.

I see plenty of headlines on the projected impact of the war on the US consumer.

Yet where is the headline, “Changes in XYZ’s cash flow statement”? (Snooze fest.) - From what I have seen, the odds of getting macro calls consistently right are incredibly low. (And I've had years of experience “observing” this topic.)

However, the experts will confidently keep making big macro calls, as long as people keep reading them.

Howard Marks highlights this in his celebrated piece “The Folly of Certainty.”1

Meanwhile, my hypothetical headline is empirical and far more important in determining XYZ's stock return. - On April 16th, 2026, Leslie and I produced our Q1 performance review and market outlook update webinar.

As I pointed out, I was not happy with AEA’s2 Q1 performance for all strategies:

What’s amazing to me—I’ve been in this business a long time—I don’t think I’ve ever seen this before: here are our top 10 stocks in Global Concentrated. Every one of them, when they reported their fourth-quarter numbers in January, beat their numbers. And their estimates were all raised by consensus by Wall Street, and yet most of them lagged. In fact, 15 out of the 18 stocks in Global Concentrated beat—yet (the strategy) didn’t do very well in the first quarter.

What we see is the “E’s” (earnings) have been going up, and yet stock prices haven’t. I really feel it’s an opportunity: I’m comforted by how many of these companies have delivered on earnings. The market has been focused on macro issues, and once those recede—as it looks like they have in the last few weeks— that gives us more comfort.”3 - In essence, investors were so consumed by the macro narrative in the first quarter, they took their eye off what ultimately drives stocks: the micro.

However, in April, another quarter of superb earnings swung investors’ attention back to the micro.

The result?

The Applied Equity Team had one of its best months ever.

- Now that the market has had a stellar month based on the micro, have investors gone too far in forgetting about the macro issues?

That makes me nervous. - We need to remember that changes in the macro can have an impact on the micro.

Even though I do believe that’s overplayed most of the time. (If only I had a dollar for every time somebody has incorrectly predicted the demise of the US consumer….)

I suspect that once we get through Q1 earnings season, investors will revert their attention back to the macro, which will rekindle Q2 anxieties.

They have not gone away. - As I stated on the Q1 webinar, investors were overly focused on the macro and had forgotten the micro.

It seems to me now they have completely swung the other way. - Bottom line, we believe the best investment opportunities come when stock prices and fundamentals significantly deviate from one another, as they did in Q1.

Now that has corrected. - My conclusions are as follows:

- Investors emphasize the macro versus the micro far more than they should.

- When the pendulum swings to the extreme, as happened in Q1, it can create wonderful investment opportunities.

- I doubt Q1 was the last fat pitch opportunity we will see in 2026.

Andrew

The Author