Monthly Review

March was defined by a sharp escalation in geopolitical risk and a corresponding repricing across rates, energy, and credit markets. The ongoing conflict involving Iran remained the dominant macro driver, shifting investor focus away from prior themes such as AI-driven disruption toward inflation risk, growth implications, and potential supply shocks in global energy markets.

The most immediate transmission channel was energy. Oil prices rose materially during the month, reaching levels around $110 per barrel, with intramonth spikes higher, as markets priced the risk of disruption to key shipping routes such as the Strait of Hormuz and potential damage to Gulf energy infrastructure. This repricing embedded a meaningful geopolitical risk premium into energy markets and raised concerns about second-order effects on inflation and growth.

Rates markets experienced a significant and broad-based repricing. Global 10-year yields rose sharply, with the U.S. 10-year increasing 38 basis points (bps) to 4.32%, the UK up 68bps to 4.92%, and Germany up 36bps to 3.00%. This move was accompanied by a bear flattening of curves, with U.S. 2s10s flattening by 4bps and 5s30s flattening by 14bps, reflecting a shift in expectations toward tighter policy and higher term premia. Inflation expectations also moved higher, with U.S. 10-year breakevens rising 5bps to 2.31%, reinforcing the inflationary implications of elevated energy prices.

This repricing reflected a sharp shift in central bank expectations. The market removed pricing for multiple Fed cuts, while European policy expectations turned more hawkish, with the European Central Bank now pricing a more restrictive stance and the Bank of England facing renewed pressure given its inflation backdrop and energy exposure. As a result, positioning built around steep curves and carry-driven strategies was disrupted, leading to adjustments across portfolios.

Credit markets remained relatively resilient in aggregate, though spreads moved wider and dispersion increased. U.S. investment grade (IG) spreads widened modestly by 5bps to 89bps OAS, supported by strong technicals including fund inflows and low dealer inventories. In contrast, Euro investment grade underperformed more materially, widening 14bps to 97bps OAS, reflecting greater macro sensitivity and weaker supply dynamics. Within IG, widening was more pronounced in lower-quality segments, with BBB spreads widening 6bps in the U.S. and 17bps in Europe.

At the same time, dispersion within IG remained elevated. M&A activity in sectors such as food & beverage and healthcare/pharmaceuticals contributed to idiosyncratic spread moves, while AI-related concerns continued to weigh on parts of the market. Some individual issuers tightened by 10–20bps during March, though these names generally remain 20–40bps wider year-to-date, underscoring that improvements have been selective rather than broad-based.

High yield markets experienced greater volatility. U.S. high yield spreads widened 26bps to 317bps, while Euro high yield widened 53bps to 332bps, with dispersion across sectors driven by both macro and idiosyncratic factors. Energy outperformed amid higher oil prices, while more cyclical sectors such as airlines lagged. Lower-quality segments underperformed meaningfully, with CCC spreads widening over 100bps in both regions.

In leveraged loans, performance stabilized following earlier weakness, particularly within software, which had been under pressure due to AI-related concerns. CLO issuance remained robust, with Q1 volumes tracking toward annualized levels consistent with the prior year, even as retail outflows persisted and managers reduced exposure to more vulnerable sectors.

Securitized markets experienced volatility primarily driven by rates. Agency MBS yields rose sharply (up ~56bps), while spreads widened modestly before partially retracing. Credit-sensitive securitized sectors saw more contained moves, with AAA spreads widening only 4–6bps, broadly returning to levels seen at the start of the year. Despite rate-driven volatility, funding conditions remained orderly.

Emerging markets reflected the broader macro repricing. EM external spreads widened ~25bps, with larger moves in high yield (+42bps) and regional dispersion across Africa (+55bps) and Europe (+44bps). Local rates also sold off meaningfully, with front-end yields in some markets rising 75–150bps, while currencies broadly weakened against the U.S. dollar, which appreciated ~2.4% over the month.

Municipal markets also adjusted to the higher rate environment, with intermediate ratios moving closer to historical averages, while the long end remained relatively well supported.

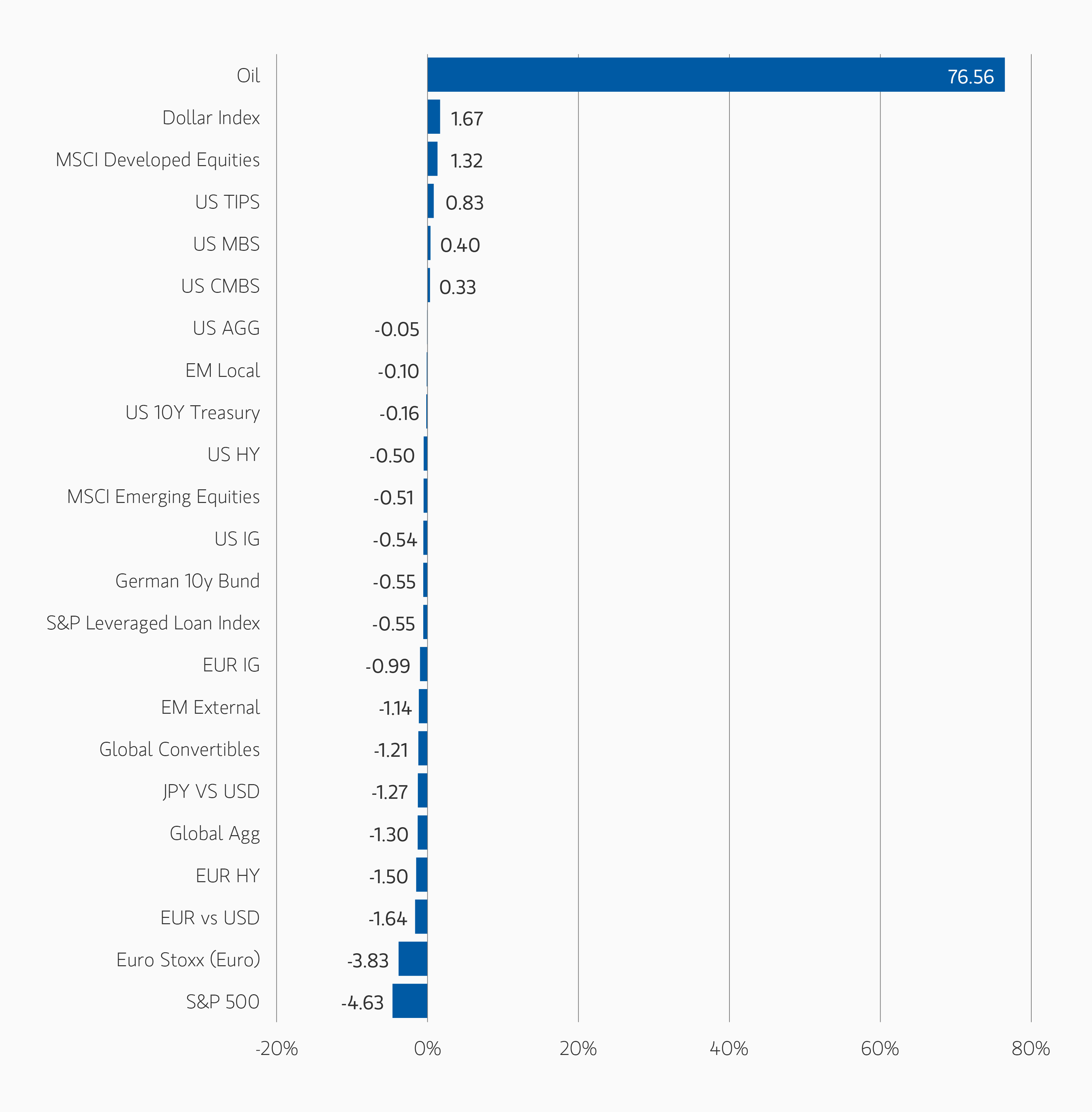

Asset Performance Year-to-Date

Asset Performance Year-to-Date

DISPLAY 1

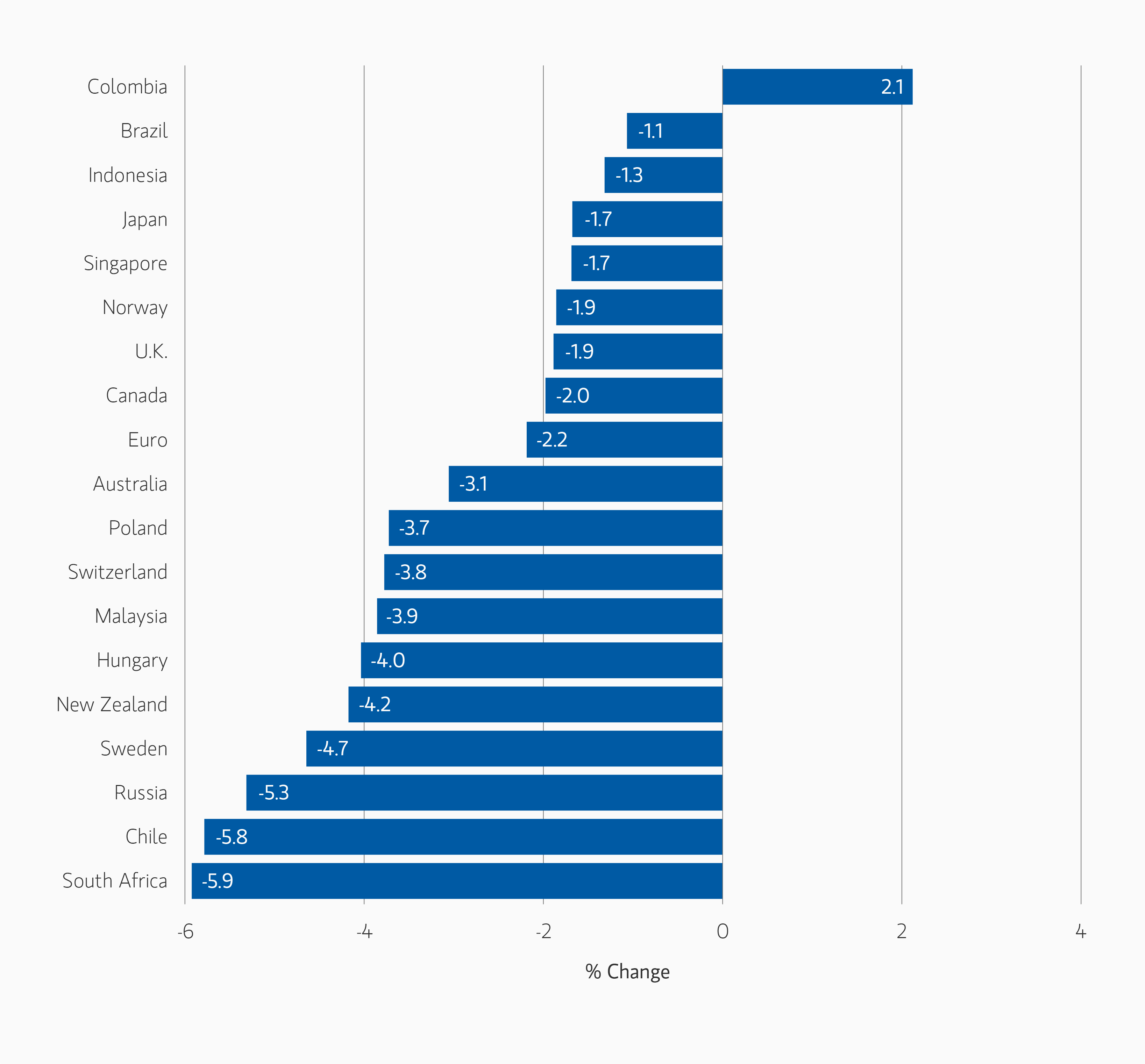

Currency Monthly Changes versus USD

Currency Monthly Changes versus USD

DISPLAY 2

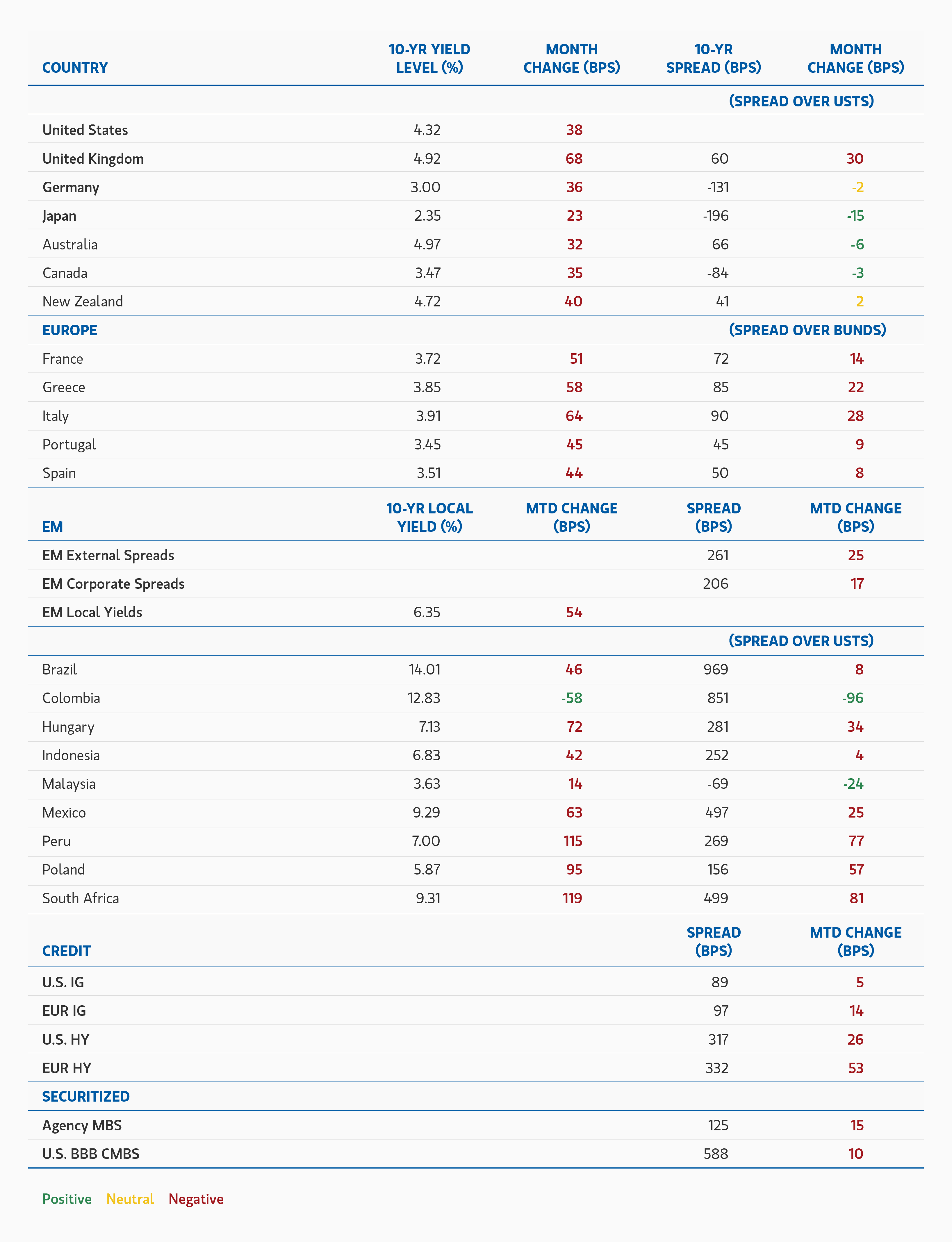

Major Monthly Changes in 10-Year Yields and Spreads

Major Monthly Changes in 10-Year Yields and Spreads

DISPLAY 3

Broad Markets Fixed Income Global Asset Allocation and Outlook

Developed Market Rate/Foreign Currency

(Long duration, curve steepeners)

February’s duration rally proved short-lived, as March saw a sharp reversal driven by a repricing of inflation and policy expectations following the escalation of the conflict in the Middle East. While markets initially reacted defensively, the persistence of elevated energy prices shifted the focus acutely towards a stagflation risk, leading to a broad selloff in rates. Despite the spike in volatility, funding markets, cross-currency basis and market depth have remained orderly.

We believe the market is over pricing the inflation shock and central bank hawkishness and underpricing the growth shock. We used the spike in volatility and yields to extend duration across selective DM and EM government markets and are now at a long duration stance across our portfolios. Global yields have moved materially higher — with the U.S. 10-year yield breaking recent ranges and real yields approaching 2%. Expectations for rate cuts have been scaled back meaningfully, while in Europe the market now prices a more restrictive policy path from the ECB. Elevated oil prices and the risk of sustained energy-driven inflation remain key risks for the global duration outlook, although inflation markets continue to suggest that any near-term increase is likely to be transitory.

Curve dynamics have also shifted, with recent moves characterized by bear flattening following earlier

steepening. We are now neutral on curves, having exited steepening exposures.

Positioning reflects a preference for relative value across regions. Our longs in U.S. real yields and Canada are offset by short positions in Japan, where normalization dynamics and weaker technicals continue to differentiate the market. Positioning in Japan remains modest but reflects asymmetric risks to yields relative to other developed markets.

In foreign exchange, we remain cautiously constructive on high-carry non-oil importing currencies. While geopolitical stress and higher oil prices have supported the U.S. dollar in the near term, we expect this strength to be episodic rather than structural. We continue to express a positive view on select high-beta FX, particularly in markets that are more insulated from the terms-of-trade and growth implications of higher energy prices. These positions are expressed primarily against the euro and the U.S. dollar.

Emerging Market Debt

(Overweight)

Emerging market (EM) sovereign and corporate debt remains an attractive opportunity for 2026, even as recent geopolitical developments and the associated rise in energy prices have introduced a more volatile macro backdrop. The spike in geopolitics led market volatility has been another reminder of how EM is not a monolithic allocation but requires careful country selection. While dispersion across countries has increased, broader EM funding conditions have remained orderly, and capital flows continue to differentiate among issuers rather than retreat indiscriminately. In this environment, carry and income remain central drivers of expected returns, though macro developments are playing a more prominent role in near-term performance.

Elevated real yields, and credible reform momentum across several countries continue to underpin a supportive backdrop. Valuations — particularly in local markets — remain attractive, and many EM currencies are still undervalued relative to the U.S. dollar. However, recent market moves have highlighted increased sensitivity to global rates and energy dynamics, with front-end yields rising in several markets and currencies experiencing periods of volatility and intervention.

The rise in oil prices has further increased divergence across the asset class, benefiting commodity exporters while posing headwinds for energy importers. As a result, dispersion across countries remains high, reinforcing the importance of policy discipline and country selection. We continue to favor markets with credible monetary frameworks, improving fundamentals, and attractive real yield differentials versus developed markets, while remaining mindful of geopolitical risks, commodity sensitivity, and evolving global policy expectations.

Corporate Credit

(More underweight IG, small overweight HY)

Our base case remains cautiously constructive for credit, even as uncertainty has increased following the escalation of the conflict in the Middle East. This view is supported by improved valuations, with spreads having decompressed from year-to-date tights, alongside expectations for low but positive economic growth and a correspondingly benign default environment. While geopolitical risks remain elevated, emerging signs of U.S. engagement aimed at de-escalation, combined with supportive fiscal policy, continue to underpin growth, employment, and consumption.

Investment grade spreads widened modestly during March, with U.S. IG moving to approximately the high-80bps range and Euro IG to the mid- to high-90bps range. While spreads remain below long-run averages, the recent widening has improved entry points, and valuations are broadly supported by strong corporate fundamentals and resilient demand for yield. At the same time, there remains limited evidence of a reactive shift in monetary policy to offset Middle East-driven inflation risks, despite markets pricing a more hawkish path for 2026.

Corporate balance sheets remain healthy as we move further into a late-cycle phase characterized by increasing M&A activity, AI- and infrastructure-related capex, and elevated shareholder distributions. This environment reinforces the importance of sector and security selection. Robust demand for the “all-in” yields offered by investment grade credit should help absorb the expected increase in issuance — particularly from non-financial corporates funding M&A and capex — though this also contributes to greater dispersion across issuers.

Given elevated geopolitical uncertainty, evolving policy expectations, and increasing idiosyncratic risk — particularly in sectors exposed to AI disruption — we have less conviction in material spread tightening from current levels. As a result, we expect carry and security selection to remain the primary drivers of return rather than broad-based multiple expansion. Regionally, we continue to prefer Europe over the U.S., supported by relatively more balanced supply dynamics and policy support.

We maintain a modest overweight to select high-yield issuers in both the U.S. and Europe. Fundamentals remain supportive, with improved average credit quality, low default rates, and manageable leverage. While spreads have widened modestly and volatility has increased, the higher carry, shorter spread duration, and continued dispersion across sectors create attractive opportunities for selective positioning. Recent market moves have reinforced the importance of quality bias and disciplined risk selection, but defaults are still expected to remain contained, supporting ongoing investor demand.

Leveraged Loans

(Underweight)

We expect heavier net supply and rising dispersion in leveraged loans. While CLO demand remains a key technical support, the asset class is increasingly characterized by greater selectivity, with managers adjusting allocations in response to evolving macro conditions and sector-specific risks. At the same time, retail flows have been more mixed, contributing to a more uneven technical backdrop.

Sector dispersion remains elevated. While software and technology-linked issuers have shown signs of stabilization following earlier weakness, structural concerns around AI-driven disruption continue to influence positioning, with CLO managers reducing exposure to the sector. More economically sensitive sectors are showing signs of strain, particularly in an environment of rising input costs and macro uncertainty.

Given the recent repricing of central bank expectations and higher rate volatility, the relative attractiveness of floating-rate assets has diminished. As a result, we maintain an underweight to the asset class, with a preference for selective exposure where fundamentals remain resilient and valuations adequately compensate for increased dispersion and macro risk.

Securitized Products

(Overweight)

Agency mortgage-backed securities (MBS) and non-agency residential mortgage-backed securities (RMBS) remain a high-conviction overweight for 2026. While agency MBS experienced periods of widening during March amid the broader rates selloff, securitized spreads remained relatively resilient overall, demonstrating stability even as volatility increased across rates markets. Agency MBS continue to offer attractive spread pickup relative to both historical levels and other core fixed income sectors, providing compelling relative value versus investment grade corporates and cash alternatives.

Recent market moves have been driven primarily by rates rather than credit fundamentals. Agency MBS yields increased materially alongside higher Treasury yields, while spread widening remained contained and partially retraced. More broadly, securitized funding markets have remained orderly, reinforcing the sector’s defensive characteristics within spread products despite elevated macro volatility.

Technical factors continue to play an important role in performance. Demand for high-quality collateral remains supported by money manager interest in carry, alongside a measured and predictable pace of Federal Reserve balance sheet runoff that has limited net supply pressure. The recent increase in yields has also improved entry points, allowing for selective addition of risk where valuations have become more attractive.

Non-agency RMBS continues to offer an attractive opportunity set, underpinned by stable home prices, low loan-to-value ratios, and historically low delinquency rates. Supply-demand dynamics remain favorable, with limited new issuance and minimal refinancing risk given the high proportion of borrowers locked into low mortgage rates.

Within CMBS, fundamentals remain resilient, particularly in higher-quality segments. Improving sentiment and stable property-level performance support selective opportunities in hospitality, logistics, storage, and high-quality multifamily assets. Dispersion across property types and geographies continues to increase, reinforcing the importance of selectivity and a focus on single-asset, single-borrower (SASB) structures.

We also remain constructive on Danish covered bonds, where defensive characteristics, strong legal frameworks, and attractive USD-hedged yields continue to support relative value.

Featured Insights