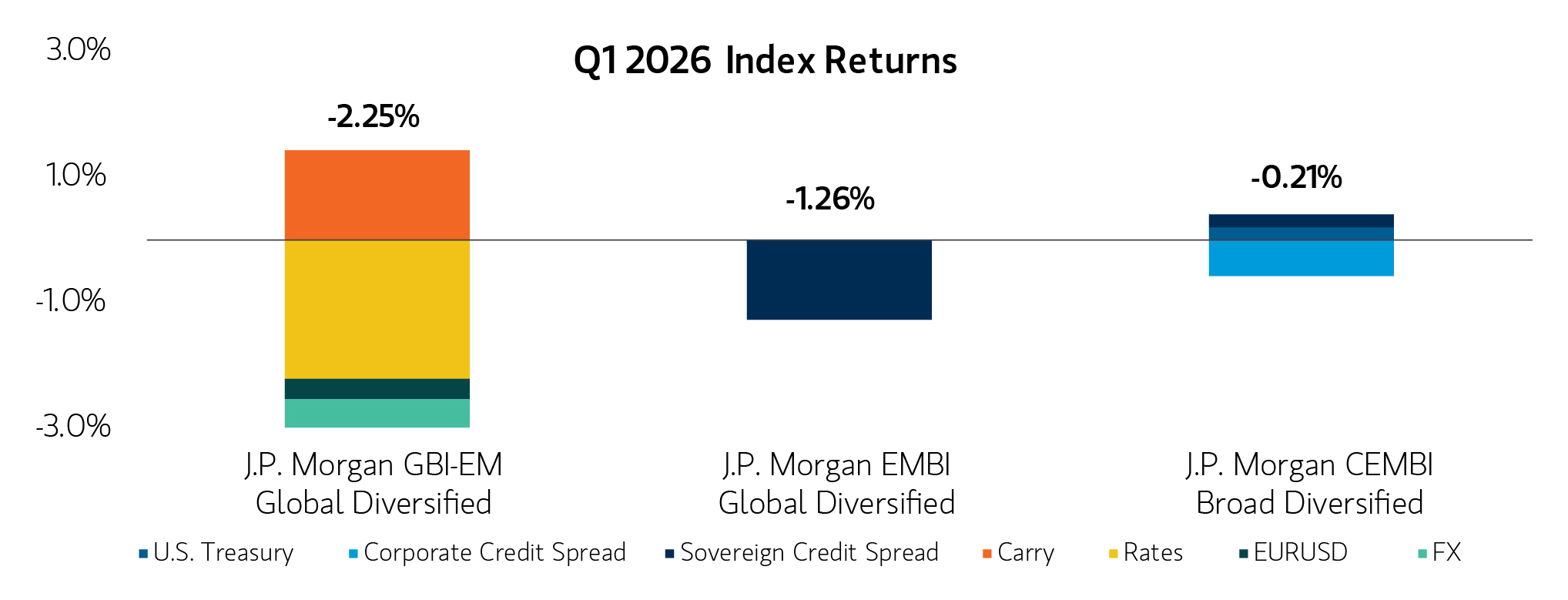

Emerging markets (EM) debt began 2026 with solid momentum, supported by favorable macro conditions and strong country fundamentals—themes that carried over from 2025. Gains in January and February were driven by a weaker U.S. dollar (USD), high real yields, spread tightening and resilient country-level fundamentals.

However, those early gains reversed in March (Display 1) after U.S. and Israeli strikes on Iran in late February sparked volatility across EMD assets. EM currencies broadly weakened against a strengthening USD, local rates came under upward pressure, and credit spreads widened across select sovereign and corporate markets.

EMD Gains Reversed in March Amid Iran-Driven Volatility

EMD Gains Reversed in March Amid Iran-Driven Volatility

Display 1

Geopolitical shifts reshape market dynamics

Key developments unfolded in the first quarter of 2026, as events in Latin America and the Middle East reshaped market dynamics both regionally and globally.

The Trump administration’s late-2025 National Security Strategy renewed focus on Latin America, paving the way for a more assertive regional posture and increased military presence in the Caribbean. Early in 2026, a high-profile U.S. operation extracted Venezuelan President Nicolás Maduro and his wife, removing him from power, with former Vice President Delcy Rodríguez assuming leadership. The new government quickly introduced sweeping economic reforms—including a revised hydrocarbons law allowing greater private participation in oil production and a cap on state royalties—that were well received by markets. These reforms helped drive a rally in Venezuelan assets through the first quarter.

In late February, coordinated U.S. and Israeli strikes targeting Iranian military sites and senior leadership sparked a rapid escalation in the conflict. Iran retaliated across the Gulf, damaging critical energy infrastructure. The effective closure of the Strait of Hormuz helped push crude oil prices above $100 per barrel at multiple points during the quarter. The conflict escalated further as Israel expanded operations against Hezbollah in southern Lebanon.

Divergent country impacts and policy responses

The resulting energy shock introduced a new layer of complexity for EM economies, with uneven effects across regions. Oil exporters outside the Middle East, including Kazakhstan, Nigeria and Colombia, benefited from higher oil prices. In contrast, energy-importing countries such as South Korea, South Africa and India faced deteriorating terms of trade, rising inflationary pressures and potential growth headwinds.

Several Southeast Asia countries introduced policy responses shortly after the conflict began to address potential oil supply disruptions. For example, Indonesia maintained fixed retail fuel prices, which increased pressure on an already strained fiscal deficit cap. Sir Lanka imposed sweeping fuel quotas and Pakistan introduced a work-from-home policy. Since March, policy responses have broadened globally, ranging from government appeals urging people to conserve electricity to more aggressive measures, such as cutting/suspending fuel taxes, travel restrictions and declaring states of emergency.

As we move beyond the initial market volatility and assess the potential medium- to long-term effects of elevated oil prices, the sustainability of these country-level policies—and the fiscal pressures they may create—will be crucial to monitor.

Outlook: An opportune time for EMD with a focus on fundamentals

Geopolitical risks have introduced volatility across select countries, reinforcing the view that the EMD investable universe is broad and highly differentiated. Rather than focusing solely on the broader market impacts of the war with Iran, investors can assess how geopolitics are influencing the opportunity set across individual countries and issuers. Trade and shipping channels have been disrupted, particularly for oil, which will likely lead to elevated oil prices for some time. The resulting shifts in terms of trade may favor oil exporters outside the Middle East, strengthening their fiscal balances and foreign exchange positions.

While pockets of the market experienced short-term volatility in March, the asset class overall remained resilient. EMD entered 2026 from a position of strength, with many countries exhibiting strong fundamentals, leaving them well positioned to manage the uncertainties surrounding inflation and growth. In this environment, central banks are likely to maintain a “higher for longer” stance, supporting attractive yield levels. The asset class is also benefiting from sustained inflows as investors continue to seek global opportunities. While flows moderated in March, strong momentum resumed in April.

Taken together, we believe the combination of resilience, differentiated opportunities and supportive yield dynamics makes a compelling case for EMD today. In this environment, rigorous bottom-up country analysis by active managers is essential to uncovering value and navigating dispersion.

Featured Insights

Index definitions:

J.P. Morgan Government Bond Index Emerging Market (JPM GBI-EM) Global Diversified is an unmanaged index of local-currency bonds with maturities of more than one year issued by emerging markets governments. Inception date for index is 12/31/2002.

J.P. Morgan Emerging Markets Bond Index Global (EMBI) Diversified Index tracks total returns for traded external debt instruments in the emerging markets, and is an expanded version of the EMBI+. As with the EMBI+, the EMBI Global includes US dollar-denominated Brady bonds, loans, and Eurobonds with an outstanding face value of at least $500 million

J.P. Morgan CEMBI Broad Diversified Index is a global, liquid corporate emerging-markets benchmark that tracks U.S.-denominated corporate bonds issued by emerging-markets entities.

Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index. Historical performance of the index illustrates market trends and does not represent the past or future performance of the fund. Information has been obtained from sources believed to be reliable, but J.P. Morgan does not warrant its completeness or accuracy. The Index is used with permission. The Index may not be copied, used, or distributed without J.P. Morgan’s prior written approval. Copyright 2026, J.P. Morgan Chase & Co. All rights reserved

RISK CONSIDERATIONS: The value of investments held by the Strategy may increase or decrease in response to economic, and financial events (whether real, expected or perceived) in the U.S. and global markets. Investments in foreign instruments or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical, currency exchange rates or other conditions. In emerging countries, these risks may be more significant. Investments in debt instruments may be affected by changes in the creditworthiness of the issuer and are subject to the risk of non- payment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. The Strategy’s exposure to derivatives involves risks different from, or possibly greater than, the risks associated with investing directly in securities and other investments. Derivatives instruments can be highly volatile, result in leverage (which can increase both the risk and return potential of the Strategy), and involve risks in addition to the risks of the underlying instrument on which the derivative is based, such as counterparty, correlation and liquidity risk. If a counterparty is unable to honor its commitments, the value of Strategy shares may decline and/or the Strategy could experience delays in the return of collateral or other assets held by the counterparty.

As interest rates rise, the value of certain income investments is likely to decline. Because the Strategy may invest significantly in a particular geographic region or country, value of Strategy shares may fluctuate more than a fund with less exposure to such areas. A non-diversified portfolio may be subject to greater risk by investing in a smaller number of investments than a diversified portfolio. Investments rated below investment grade (sometimes referred to as junk) are typically subject to greater price volatility and illiquidity than higher rated investments. The Strategy is exposed to liquidity risk when trading volume, lack of a market maker or trading partner, large position size, market conditions, or legal restrictions impair its ability to sell particular investments or to sell them at advantageous market prices. The impact of the coronavirus on global markets could last for an extended period and could adversely affect the Strategy’s performance.

IMPORANT INFORMATION

There is no guarantee that any investment strategy will work under all market conditions, and each investor should evaluate their ability to invest for the long-term, especially during periods of downturn in the market.

A separately managed account may not be appropriate for all investors. Separate accounts managed according to the Strategy include a number of securities and will not necessarily track the performance of any index. Please consider the investment objectives, risks and fees of the Strategy carefully before investing. A minimum asset level is required.

For important information about the investment managers, please refer to Form ADV Part 2.

The views and opinions and/or analysis expressed are those of the author or the investment team as of the date of preparation of this material and are subject to change at any time without notice due to market or economic conditions and may not necessarily come to pass. Furthermore, the views will not be updated or otherwise revised to reflect information that subsequently becomes available or circumstances existing, or changes occurring, after the date of publication. The views expressed do not reflect the opinions of all investment personnel at Morgan Stanley Investment Management (MSIM) and its subsidiaries and affiliates (collectively “the Firm”), and may not be reflected in all the strategies and products that the Firm offers.

Forecasts and/or estimates provided herein are subject to change and may not actually come to pass. Information regarding expected market returns and market outlooks is based on the research, analysis and opinions of the authors or the investment team. These conclusions are speculative in nature, may not come to pass and are not intended to predict the future performance of any specific strategy or product the Firm offers. Future results may differ significantly depending on factors such as changes in securities or financial markets or general economic conditions.

This material has been prepared on the basis of publicly available information, internally developed data and other third-party sources believed to be reliable. However, no assurances are provided regarding the reliability of such information and the Firm has not sought to independently verify information taken from public and third-party sources.

This material is for the benefit of persons whom the Firm reasonably believes it is permitted to communicate to and should not be forwarded to any other person without the consent of the Firm. It is not addressed to any other person and may not be used by them for any purpose whatsoever. It expresses no views as to the suitability of the investments described herein to the individual circumstances of any recipient or otherwise. It is the responsibility of every person reading this material to fully observe the laws of any relevant country, including obtaining any governmental or other consent which may be required or observing any other formality which needs to be observed in that country. Unless otherwise stated, returns and market values contained herein are presented in US dollars.

This material is a general communication, which is not impartial and all information provided has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy. The information herein has not been based on a consideration of any individual investor circumstances and is not investment advice, nor should it be construed in any way as tax, accounting, legal or regulatory advice. To that end, investors should seek independent legal and financial advice, including advice as to tax consequences, before making any investment decision.

The Firm does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. It was not intended or written to be used, and it cannot be used by any taxpayer, for the purpose of avoiding penalties that may be imposed on the taxpayer. Each Jurisdiction tax laws are complex and constantly changing. You should always consult your own legal or tax professional for information concerning your individual situation.

Any charts and graphs provided are for illustrative purposes only. Past performance does not guarantee future results.

The Firm has not authorised financial intermediaries to use and to distribute this material, unless such use and distribution is made in accordance with applicable law and regulation. Additionally, financial intermediaries are required to satisfy themselves that the information in this material is appropriate for any person to whom they provide this material in view of that person’s circumstances and purpose. The Firm shall not be liable for, and accepts no liability for, the use or misuse of this material by any such financial intermediary.

This material may be translated into other languages. Where such a translation is made this English version remains definitive. If there are any discrepancies between the English version and any version of this material in another language, the English version shall prevail.

The whole or any part of this material may not be directly or indirectly reproduced, copied, modified, used to create a derivative work, performed, displayed, published, posted, licensed, framed, distributed or transmitted or any of its contents disclosed to third parties without the Firm’s express written consent. This material may not be linked to unless such hyperlink is for personal and non-commercial use. All information contained herein is proprietary and is protected under copyright and other applicable law.

Eaton Vance is part of Morgan Stanley Investment Management. Morgan Stanley Investment Management is the asset management division of Morgan Stanley.

DISTRIBUTION

This material is only intended for and will only be distributed to persons resident in jurisdictions where such distribution or availability would not be contrary to local laws or regulations.

MSIM, the asset management division of Morgan Stanley (NYSE: MS), and its affiliates have arrangements in place to market each other’s products and services. Each MSIM affiliate is regulated as appropriate in the jurisdiction it operates. MSIM’s affiliates are: Calvert Research and Management, Eaton Vance Management, Parametric Portfolio Associates LLC, Parametric SAS, and Atlanta Capital Management LLC.

This material has been issued by any one or more of the following entities:

EMEA

This material is for Professional Clients/Accredited Investors only.

In the EU, MSIM materials are issued by MSIM Fund Management (Ireland) Limited (“FMIL”). FMIL is regulated by the Central Bank of Ireland and is incorporated in Ireland as a private company limited by shares with company registration number 616661 and has its registered address at 24-26 City Quay, Dublin 2, DO2 NY19, Ireland.

Outside the EU, MSIM materials are issued by Morgan Stanley Investment Management Limited (MSIM Ltd) is authorised and regulated by the Financial Conduct Authority. Registered in England. Registered No. 1981121. Registered Office: 25 Cabot Square, Canary Wharf, London E14 4QA.

In Switzerland, MSIM materials are issued by Morgan Stanley & Co. International plc, London (Zurich Branch) Authorised and regulated by the Eidgenössische Finanzmarktaufsicht ("FINMA"). Registered Office: Beethovenstrasse 33, 8002 Zurich, Switzerland.

Italy: MSIM FMIL (Milan Branch), (Sede Secondaria di Milano) Palazzo Serbelloni Corso Venezia, 16 20121 Milano, Italy. The Netherlands: MSIM FMIL (Amsterdam Branch), Rembrandt Tower, 11th Floor Amstelplein 1 1096HA, Netherlands. France: MSIM FMIL (Paris Branch), 61 rue de Monceau 75008 Paris, France. Spain: MSIM FMIL (Madrid Branch), Calle Serrano 55, 28006, Madrid, Spain. Germany: MSIM FMIL Frankfurt Branch, Große Gallusstraße 18, 60312 Frankfurt am Main, Germany (Gattung: Zweigniederlassung (FDI) gem. § 53b KWG). Denmark: MSIM FMIL (Copenhagen Branch), Gorrissen Federspiel, Axel Towers, Axeltorv2, 1609 Copenhagen V, Denmark.

MIDDLE EAST

Dubai International Financial Centre: This information does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe for or purchase, any securities or investment products in the UAE (including the Dubai International Financial Centre and the Abu Dhabi Global Market) and accordingly should not be construed as such. Furthermore, this information is being made available on the basis that the recipient acknowledges and understands that the entities and securities to which it may relate have not been approved, licensed by or registered with the UAE Central Bank, the Dubai Financial Services Authority, the UAE Securities and Commodities Authority, the Financial Services Regulatory Authority or any other relevant licensing authority or government agency in the UAE. The content of this report has not been approved by or filed with the UAE Central Bank, the Dubai Financial Services Authority, the UAE Securities and Commodities Authority or the Financial Services Regulatory Authority.

Abu Dhabi Global Market ("ADGM"): This material is sent strictly within the context of, and constitutes, an Exempt Communication. This material relates to emerging markets debt, which is not subject to any form of regulation or approval by the Financial Services Regulatory Authority of the Abu Dhabi Global Market (the “FSRA”).

Saudi Arabia

This financial promotion was issued and approved for use in Saudi Arabia by Morgan Stanley Saudi Arabia, Al Rashid Tower, Kings Sand Street, Riyadh, Saudi Arabia, authorized and regulated by the Capital Market Authority license number 06044-37.

U.S.

NOT FDIC INSURED | OFFER NO BANK GUARANTEE | MAY LOSE VALUE | NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY | NOT A DEPOSIT

Latin America (Brazil, Chile Colombia, Mexico, Peru, and Uruguay)

This material is for use with an institutional investor or a qualified investor only. All information contained herein is confidential and is for the exclusive use and review of the intended addressee, and may not be passed on to any third party. This material is provided for informational purposes only and does not constitute a public offering, solicitation or recommendation to buy or sell for any product, service, security and/or strategy. A decision to invest should only be made after reading the strategy documentation and conducting in-depth and independent due diligence.

ASIA PACIFIC

Hong Kong: This document has been issued by Morgan Stanley Asia Limited, CE No. AAD291, for use in Hong Kong and shall only be made available to “professional investors” as defined under the Securities and Futures Ordinance of Hong Kong (Cap 571). The contents of this document have not been reviewed nor approved by any regulatory authority including the Securities and Futures Commission in Hong Kong. Accordingly, save where an exemption is available under the relevant law, this document shall not be issued, circulated, distributed, directed at, or made available to, the public in Hong Kong. Singapore: This material is disseminated in Singapore by Morgan Stanley Investment Management Company, Registration No. 199002743C. This material should not be considered to be the subject of an invitation for subscription or purchase, whether directly or indirectly, to the public or any member of the public in Singapore other than (i) to an institutional investor under section 304 of the Securities and Futures Act, Chapter 289 of Singapore (“SFA”), (ii) to a “relevant person” (which includes an accredited investor) pursuant to section 305 of the SFA, and such distribution is in accordance with the conditions specified in section 305 of the SFA; or (iii) otherwise pursuant to, and in accordance with the conditions of, any other applicable provision of the SFA. This material has not been reviewed by the Monetary Authority of Singapore. Australia: This material is provided by Morgan Stanley Investment Management (Australia) Pty Ltd ABN 22122040037, AFSL No. 314182 and its affiliates and does not constitute an offer of interests. Morgan Stanley Investment Management (Australia) Pty Limited arranges for MSIM affiliates to provide financial services to Australian wholesale clients. This material will not be lodged with the Australian Securities and Investments Commission.

Japan

For professional investors, this material is circulated or distributed solely for informational purposes. For non-professional investors, this material is provided in connection with Morgan Stanley Investment Management (Japan) Co., Ltd. (“MSIMJ”)’s business with respect to discretionary investment management agreements (“IMA”) and investment advisory agreements (“IAA”). This does not constitute a recommendation or solicitation of transactions nor offers any particular financial instruments. Under an IMA, with respect to the management of client assets, the client prescribes basic management policies in advance and commissions MSIMJ to make all investment decisions based on an analysis of the value, etc. of the securities, and MSIMJ accepts such commission. The client shall delegate to MSIMJ the authorities necessary to make such investment decisions. MSIMJ exercises these delegated authorities accordingly, and the client shall not make individual instructions. All investment profits and losses belong to the clients; principal is not guaranteed. Please consider the investment objectives and nature of risks before investing. As an investment advisory fee for an IAA or an IMA, the amount of assets subject to the contract multiplied by a certain rate (the upper limit is 2.20% per annum (including tax)) shall be incurred in proportion to the contract period. For some strategies, a contingency fee may be incurred in addition to the fee mentioned above. Indirect charges also may be incurred, such as brokerage commissions for underlying securities. Since these charges and expenses vary by contract and other factors, MSIMJ cannot present the rates, upper limits, etc. in advance. All clients should read thoroughly the Documents Provided Prior to the Conclusion of a Contract carefully before executing an agreement. This material is distributed in Japan by MSIMJ, Registered No. 410 (Director of Kanto Local Finance Bureau (Financial Instruments Firms)), Membership: the Japan Securities Dealers Association, the Investment Management Association of Japan and the Type II Financial Instruments Firms Association.