In the fourth quarter, emerging markets (EM) debt capped a year of exceptionally strong performance with positive returns in both hard currency and local currency debt. EM debt was supported by a weakening U.S. dollar, easing monetary policy by many EM central banks, tightening credit spreads and ongoing investor demand for non-dollar assets.

Looking ahead, several factors are driving our constructive outlook for 2026 for EM debt: Robust investor demand for non-dollar assets, EM real yields that continue to exceed those in developed markets, an ongoing favorable inflation picture in most EM countries, and strong fundamentals in select countries.

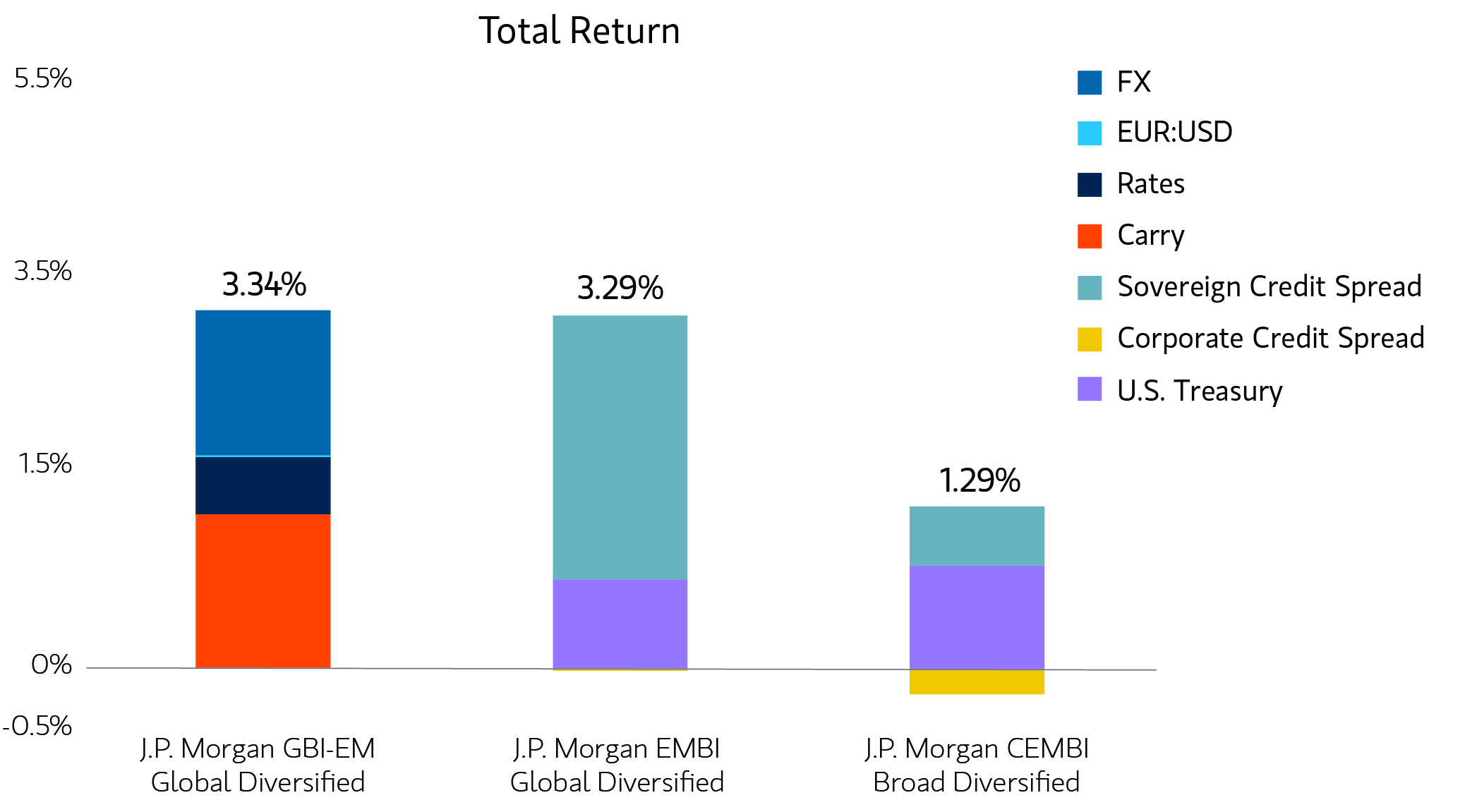

A strong finish to 2025

Display 1 shows the significant contributions to return in the fourth quarter from foreign exchange and interest rates for local currency debt. The hard currency sectors benefitted from spread tightening and U.S. Treasury gains. Reduced inflation expectations helped drive rates lower. Mixed, but broadly improving fundamentals, drove both spread tightening and currency appreciation, which was helped by the tailwind of a weakening U.S. dollar.

FX, spread compression and falling rates power 4Q EM debt returns.

FX, spread compression and falling rates power 4Q EM debt returns.

Display 1

Fourth quarter developments

World debt markets were buoyed by the broad trend toward lower policy rates. The U.S. Federal Reserve lowered its policy rate by 25 basis points (bps) twice, and nine other central banks also eased. (The Bank of Japan being the lone exception.)

Improving investor sentiment toward non-U.S. assets helped spark inflows of $13.2 billion into the asset class -- $6.4 billion for the hard currency segment and $6.8 billion for local currency.

In macro developments, the U.S. and China established an updated trade deal in November, with both sides making concessions set to expire in November 2026. Global strategic and economic realignment continued on several other fronts -- India sought to establish free trade agreements with the European Union, New Zealand, Chile and Oman, and trade was also the theme at the G20 Johannesburg summit, the Asia-Pacific Economic Cooperation (APEC) summit in Korea, and the European Union-African Union summit in Angola.

Elsewhere, the EU approved a €90 billion aid package for Ukraine, and while the ceasefire between Israel and Hamas held, both sides have accused each other of breaching it. The political party of Argentinian president Javier Milei – a strong ally of President Trump – won a decisive victory in midterm elections, prompting a short-lived rally in the peso.

2026 outlook

- The timing and magnitude of future Fed cuts are uncertain as the Fed manages delayed economic data, increasing unemployment, and inflation levels. For many EM countries average inflation is likely to continue to fall relative to developed markets, and support the real yield differential that favors EM debt. Select EM central banks will be positioned to continue to cut rates.

- Demand for the asset class is likely to continue following strong returns in 2025 and attractive valuations plus improving fundamentals. The weakening U.S. dollar and ongoing U.S. policy uncertainty should also support demand for non-dollar assets. Despite strong gains in 2025, EM currencies are still cheap compared with long term averages.

- EM countries will continue to negotiate tariff policies with the U.S., and some are starting to feel the impact. Key elections to watch include presidential contests in Brazil, Colombia, and Peru, as well as major parliamentary elections in Hungary, Lebanon, Israel, and Armenia.

- Geopolitical stress points from Russia-Ukraine, Israel-Hamas and Venezuela continue to be sources of uncertainty that could have trickle-down effects on the world economy.

By maintaining our ongoing focus on individual country fundamentals and policy responses, we believe our strategies will be well-positioned to uncover value and capitalize on the factors driving today’s markets.

Analyses mises en avant