Constructive and Cautious Amid a Fluid Backdrop

Performance is increasingly driven by structural growth drivers rather than cyclical market exposure”

Key Reflections

The current macro environment is defined by resilience amid volatility and growing divergence across regions and sectors. Despite geopolitical tensions, elevated inflation and tighter monetary policy, growth has remained durable—particularly in the U.S. and parts of Asia and Europe—which supports real estate fundamentals. The recent meaningful repricing of ~20–25% provides an attractive point of entry, while constrained supply and higher construction costs underpin real estate fundamentals.

At the same time, performance is increasingly driven by structural growth drivers rather than cyclical market exposure. Secular themes such as AI, deglobalization, demographic shifts and energy demand are creating clear winners and laggards. This environment reinforces the importance of selectivity, diversification and active capital allocation to capture emerging pockets of outperformance.

What We Are Seeing

We are seeing global growth remain intact despite macro and geopolitical headwinds, with strong nominal expansion in the U.S., Japan, Korea and pockets of Europe that support real estate demand. Inflation remains persistent, driving a more hawkish policy stance and keeping interest rates structurally higher. This has increased the cost of capital while simultaneously constraining new supply, as development becomes less economically viable.

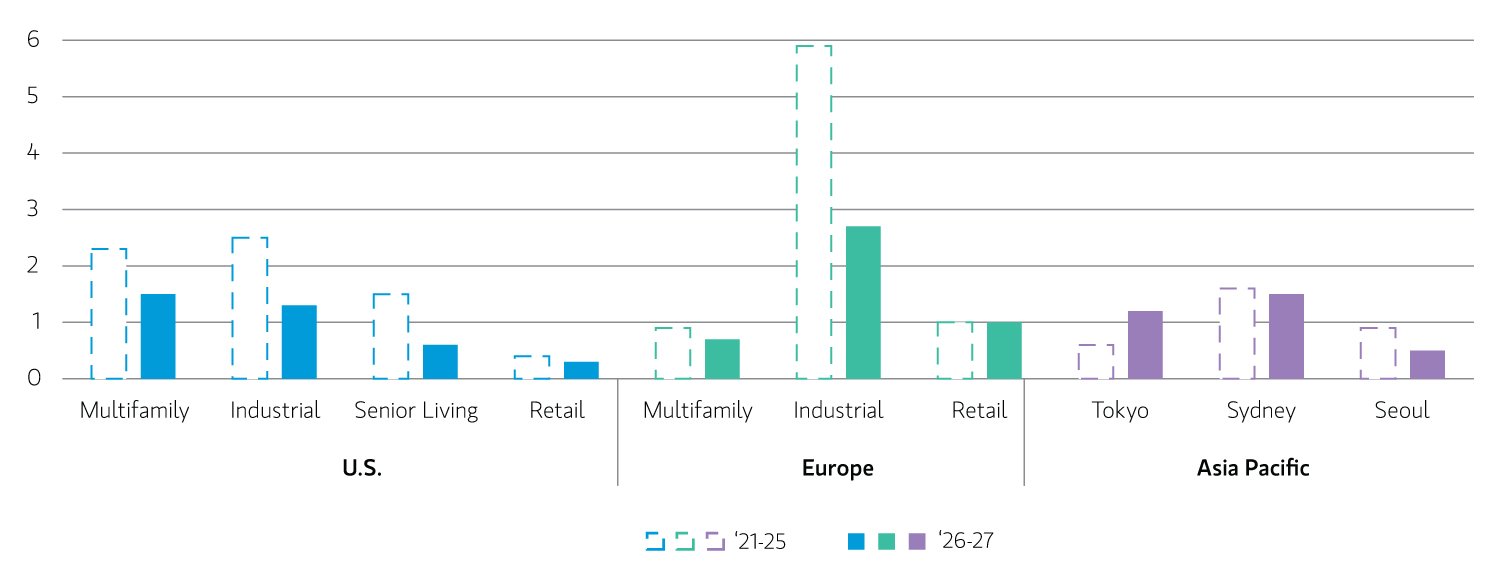

Real estate markets are reflecting this shift, with capital flows and transaction activity rebounding as investors seek relative value. Pricing has corrected meaningfully since 2022, and yields are at multi-year highs. However, performance dispersion is widening, with sectors that are tied to long-term growth themes—such as senior housing, industrial and supply-constrained residential—continuing to outperform through stronger rent growth.

What We Are Doing

In the current environment, we are focused on deploying capital into assets that combine attractive entry pricing with durable, long-term demand drivers. This includes acquiring assets at a discount to replacement cost in supply-constrained markets, particularly in areas that are aligned with key secular themes such as AI infrastructure, reshoring-driven logistics, aging demographics and energy-related demand.

In the U.S., we are focused on both the industrial and residential sectors, driven respectively by AI-led demand and favorable demographic trends. On the industrial side, we are prioritizing distribution assets within data center clusters and advanced manufacturing facilities supported by expanding defense spending and physical AI. On the residential side, we are targeting senior housing aligned with aging demographics, alongside multifamily and student housing in markets with compelling demand–supply imbalances. In Europe, we continue to prioritize residential investments in markets characterized by structurally constrained supply. Additionally, elevated financing costs and reduced liquidity are placing pressure on existing owners to deleverage or return capital, creating attractive opportunities for recapitalizations. In Asia, we see compelling opportunities across Japan, Korea and Australia, where strong domestic demand—supported by AI- and technology-led exports as well as favorable demographic trends—is driving growth in both residential and industrial sectors. In Japan specifically, ongoing corporate governance reforms are unlocking value, creating opportunities to acquire non-core assets across all sectors.

At the portfolio level, we are emphasizing diversification and flexibility, enabling dynamic capital allocation across geographies and sectors. A strong focus on asset-level selection remains critical, where we target properties with the specifications, locations and operating profiles that align with evolving occupier needs. This disciplined, granular approach is central to capturing differentiated returns.

What We Are Watching

We are closely monitoring the path of inflation and interest rates, which will continue to shape valuation and liquidity dynamics. The timing and extent of any normalization of monetary policy remains uncertain, while geopolitical risks—particularly in energy markets—could introduce further volatility and impact global growth trajectories.

In addition, we are tracking how structural trends translate into real estate demand, including the pace of AI deployment, defense spending and demographic shifts. Supply dynamics remain a key variable, as today’s constrained pipeline supports fundamentals, but any future rebound in development could influence medium-term rent growth. Together, these factors will determine the durability of current tailwinds and investment opportunities that lie ahead.

Reduced Supply Supports Fundamentals

Source: Greenstream, Oxford Economics, June 2026. Note Asia cities represent average across sectors, historical = ‘24-25 and forecast ‘26-27.

Reduced Supply Supports Fundamentals

Annual Supply Growth (%)

Featured Insights