Monthly Review

May was marked by continued U.S. economic resilience, persistent inflation concerns, and a further repricing of monetary policy expectations, even as risk assets remained well-supported. Stronger-than-expected payrolls and unemployment near 4.3% pointed to a still-tight labor market, while firm consumption was supported by wealth effects from stronger equity markets and continued fiscal impulse. Inflation remained a key focus, with core CPI rising from its February lows and strong PPI data raising concerns around eventual pass-through into PCE.

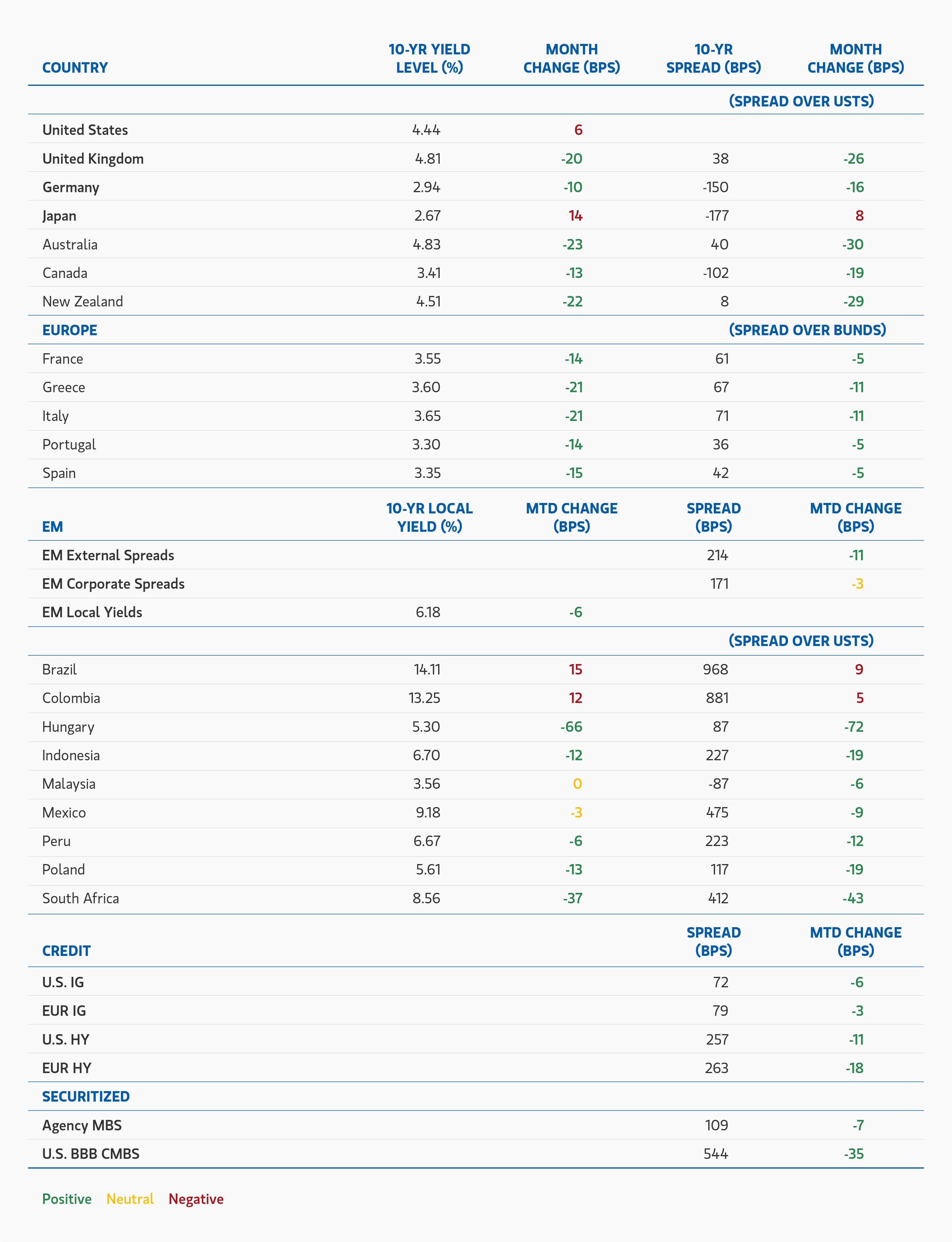

Rates markets reflected this more resilient growth and sticky inflation backdrop. The U.S. 10-year yield rose 6 basis points (bps) to 4.44%, while Japan also saw yields move higher. By contrast, several other developed markets rallied, with UK, Canada, Australia, and New Zealand yields declining. U.S. 10-year breakevens fell 9bps, suggesting some moderation in market-implied inflation expectations even as inflation risks remained central to the macro discussion. The U.S. dollar strengthened modestly, with ICE U.S. Dollar Index up 0.9%.

Credit markets remained resilient despite tight valuations. U.S. investment grade (IG) spreads tightened 6 bps to 72 bps, while Euro IG tightened 3 bps to 79 bps. Carry remained the dominant driver of returns, supported by exceptionally strong technicals and continued demand for all-in yield. Both U.S. and European markets absorbed record issuance with little disruption, as strong inflows and healthy investor demand offset elevated supply. In Europe, May marked the largest issuance month on record, while U.S. issuance also exceeded expectations, with the vast majority of new deals tightening in secondary trading. A notable theme was the continued acceleration of AI-related financing, particularly among large technology and hyperscale issuers, reinforcing expectations that infrastructure spending will remain an important driver of corporate issuance. High yield also performed well, with U.S. High Yield (HY) tightening 11 bps to 257 bps and Euro HY tightening 18 bps to 263 bps. Despite the constructive backdrop, valuations remain tight and dispersion persists across sectors, reinforcing the importance of security selection.

Leveraged loans delivered solid performance, supported by strong earnings and healthy CLO demand. Software loans stabilized after earlier weakness tied to AI disruption concerns, though the sector continued to lag year-to-date. Investors remained focused on higher-quality, mission-critical issuers, while housing, lower-income consumer, and packaging exposures showed more strain.

Securitized markets were supported by strong demand and improving technicals. Agency Mortgage-Backed Securities (MBS) spreads tightened as rate volatility eased, while bank and GSE demand helped offset Fed balance sheet runoff. Securitized credit issuance remained robust across Residential MBS (RMBS), Asset-Backed Securities (ABS), and Commercial MBS (CMBS), with residential credit continuing to stand out on stable collateral performance and strong investor demand.

Emerging markets (EM) were mixed but broadly constructive. EM external spreads tightened 11 bps to 215 bps, with support from select Latin American markets and improving political developments in Colombia. Asia faced more inflation and currency pressure, including Indonesia’s rate hike and export restrictions. Oil-linked risk premia remained relevant given still-low vessel traffic through the Strait of Hormuz.

Municipals continued to perform strongly, supported by substantial inflows and favorable technicals despite record issuance. High yield munis remained one of the stronger areas of U.S. fixed income, helped by limited supply and strong demand.

Overall, May reinforced the resilience of risk markets despite sticky inflation, tighter policy expectations, and ongoing geopolitical uncertainty. Technical demand remained a powerful support, but tight valuations and rising dispersion continued to place a premium on sector allocation and security selection.

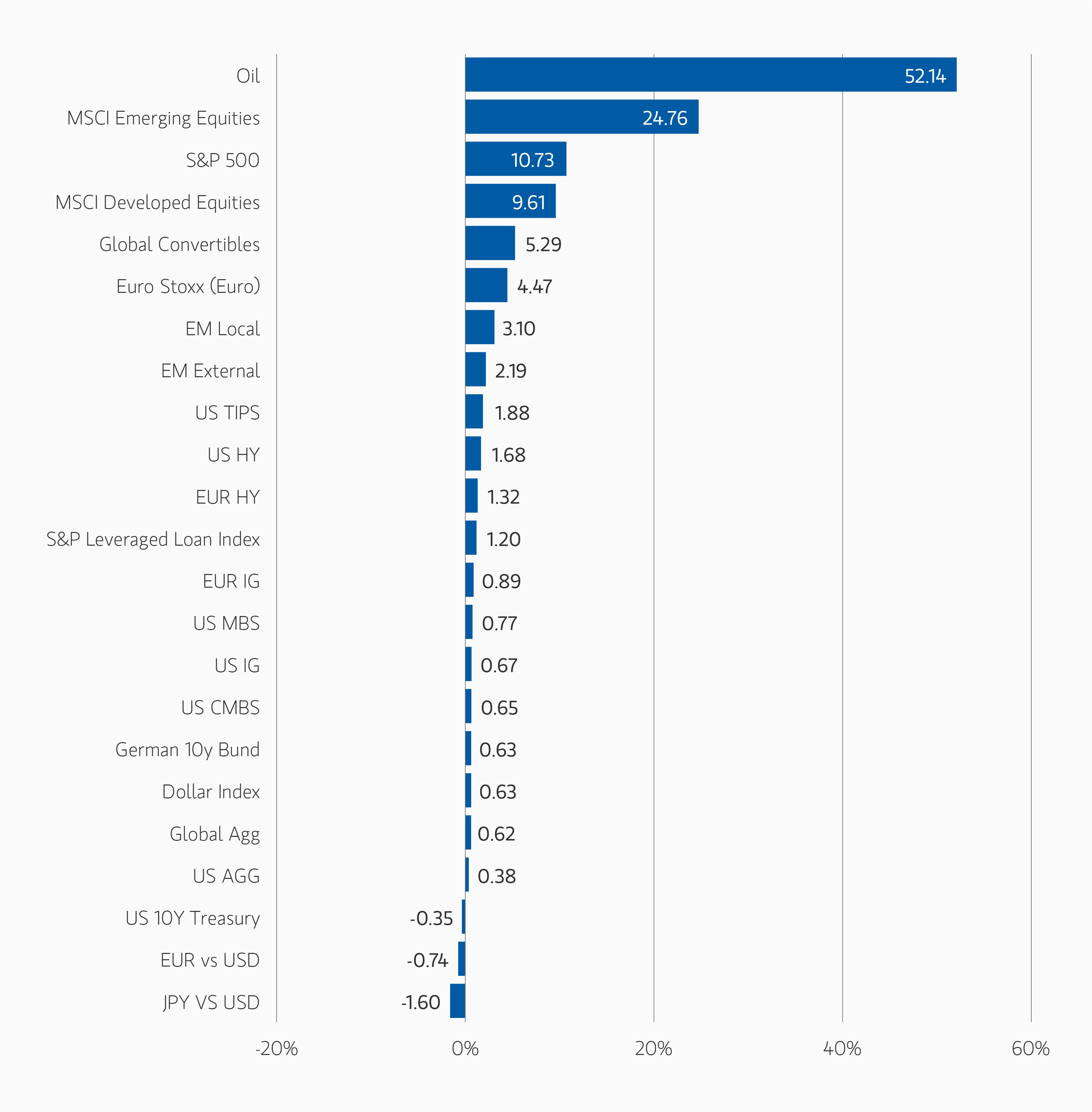

Asset Performance Year-to-Date

Asset Performance Year-to-Date

DISPLAY 1

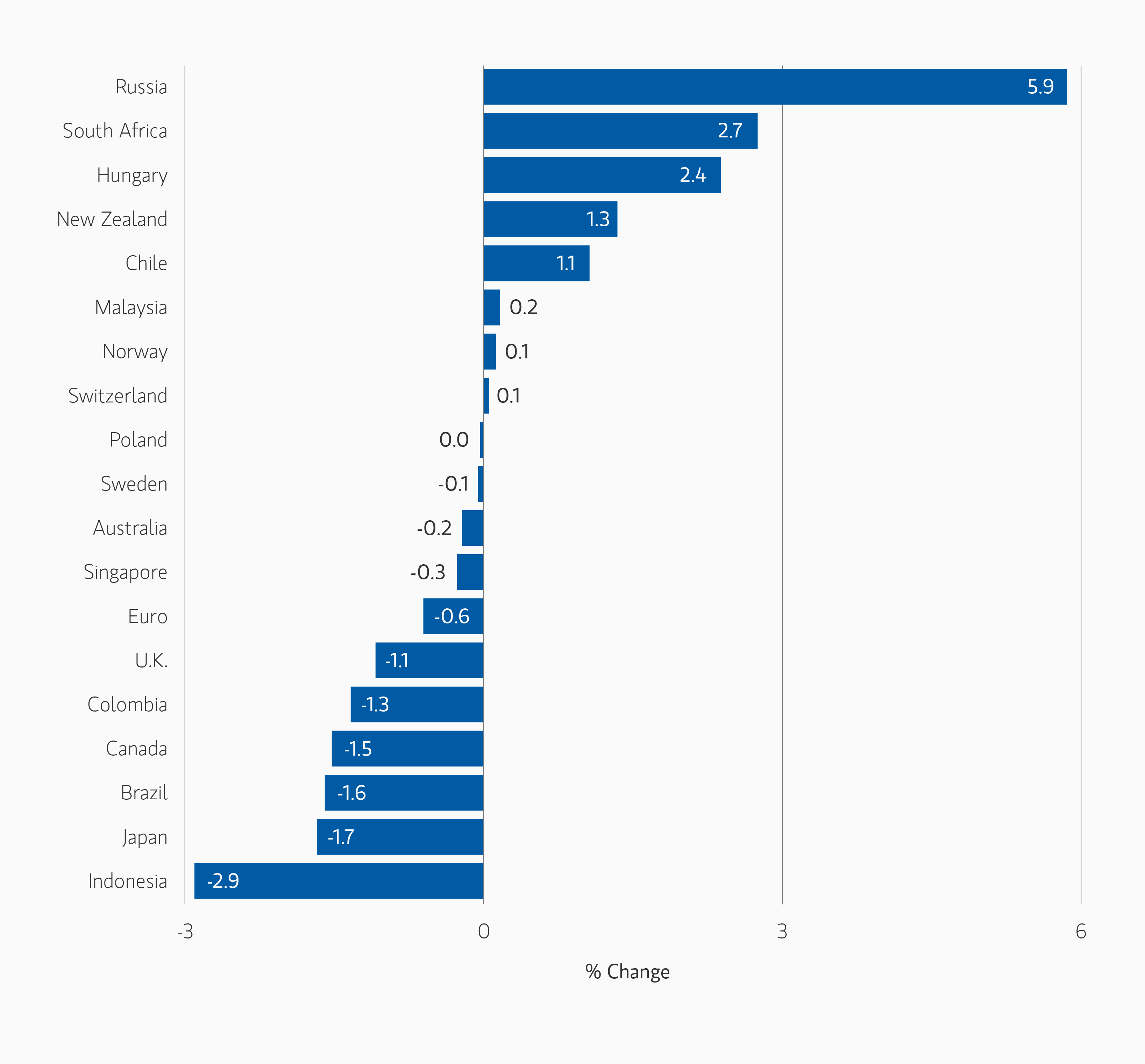

Currency Monthly Changes versus USD

Currency Monthly Changes versus USD

DISPLAY 2

Major Monthly Changes in 10-Year Yields and Spreads

Major Monthly Changes in 10-Year Yields and Spreads

DISPLAY 3

Broad Markets Fixed Income Global Asset Allocation and Outlook

Developed Market Rate/Foreign Currency

(Long duration, neutral curve positioning)

The market narrative has continued to shift away from recession concerns and toward the durability of growth and inflation. In the United States, stronger-than-expected labor market data, resilient consumption, and firm inflation readings have led investors to significantly reprice monetary policy expectations, with markets now anticipating a much more restrictive policy path than was expected at the beginning of the year. Elsewhere in developed markets, much of this repricing occurred earlier in the year, though inflation and energy-related risks continue to influence central bank expectations. While geopolitical developments remain an important driver of sentiment, the dominant macro question has become whether inflation proves sufficiently persistent to delay or reverse the easing cycle.

Against this backdrop, we continue to maintain a long duration stance across developed markets, though positioning remains highly selective and focused on regions where growth appears more vulnerable to tighter financial conditions. Exposure is concentrated in front-end rates markets outside the United States, alongside a long position in U.S. Treasuries. We have moderated some exposure in Canada following recent developments and weaker growth data, while continuing to favor markets where economic momentum appears less robust than in the U.S. Duration exposure remains partially offset by short positions in markets where policy normalization and technical dynamics create asymmetric upside risks to yields.

Inflation remains the primary macro risk. Although longer-dated inflation expectations retraced modestly during May, core inflation measures have continued to move higher and producer price pressures remain firm. We therefore maintain meaningful exposure to U.S. inflation-linked markets, where we continue to see value in hedging portfolios against the risk that inflation remains above central bank targets for longer than currently anticipated.

Curve dynamics have generally stabilized following the sharp repricing seen earlier in the year, and we remain neutral on outright curve positioning. While elevated fiscal deficits, AI-related investment spending, and energy market uncertainty continue to support higher term premia over the medium term, recent moves have reduced the attractiveness of directional curve expressions.

In foreign exchange, we continue to favor selective high-carry currencies where fundamentals and valuation remain supportive. Positioning is focused on the Mexican peso and Hungarian forint against the euro, reflecting attractive carry characteristics and differentiated domestic drivers. More broadly, we expect currency markets to remain highly sensitive to evolving central bank expectations, energy prices, and geopolitical developments, with relative growth and inflation dynamics continuing to drive performance across developed and emerging markets.

Emerging Market Debt

(Overweight)

Emerging market sovereign and corporate debt remains an attractive opportunity, supported by elevated real yields, resilient technicals, and improving fundamentals in select countries. Despite persistent geopolitical uncertainty and a more hawkish global policy backdrop, EM credit markets have remained broadly resilient, with spreads continuing to retrace toward pre-conflict levels in several regions.

Carry and income remain central drivers of expected returns, though country selection remains critical given elevated dispersion across regions. Higher energy prices continue to create divergence between commodity exporters and importers, while local political developments remain an important source of idiosyncratic opportunity and risk. Recent developments in markets such as Colombia, Hungary, Indonesia, and the Philippines highlight the increasingly differentiated nature of the opportunity set.

Valuations remain attractive across select local and hard-currency markets, and many EM currencies continue to offer compelling carry relative to developed markets. While tighter global financial conditions and persistent inflation remain important risks, we continue to favor countries with credible monetary frameworks, improving fundamentals, and attractive real yield differentials. In an environment where global growth remains positive and default risks remain contained, we believe the asset class continues to offer attractive risk-adjusted return potential.

Corporate Credit

(Underweight IG, small overweight HY)

Our base case remains cautiously constructive for credit, even as inflation risks, tighter monetary policy expectations, and geopolitical uncertainty continue to shape the macro backdrop. Despite these headwinds, resilient economic growth, strong labor markets, and continued fiscal support have helped sustain corporate fundamentals and support demand for risk assets.

We continue to believe that a meaningful demand destruction scenario is unlikely to be the base case. Expectations for low but positive economic growth—supported by ongoing fiscal support, energy-related spending, and continued AI and infrastructure investment—remain consistent with a broadly benign default environment. Corporate balance sheets also remain healthy, though the market is increasingly entering a late-cycle phase characterized by elevated M&A activity, AI- and infrastructure-related capex, and higher shareholder distributions. This backdrop reinforces the importance of sector and security selection.

At current spread levels, we continue to view carry as the primary driver of expected returns, supported by strong technical demand for high-quality credit and resilient corporate fundamentals. Demand for all-in yield remains robust, helping absorb elevated issuance volumes and supporting spread stability despite tight valuations. While broad-based spread compression appears increasingly limited, we continue to see opportunities for excess return through sector allocation and security selection. Regionally, we continue to prefer Europe over the U.S., supported by relatively more balanced supply dynamics and stronger demand for high-quality carry.

We maintain a modest overweight to select high-yield issuers in both the U.S. and Europe. Although spreads remain historically tight and issuance has accelerated, fundamentals remain supportive, with improved average credit quality, manageable leverage, and contained default expectations. Elevated dispersion across sectors and issuers continues to create opportunities for selective positioning, particularly in businesses with resilient cash flows, stronger pricing power, and less exposure to refinancing risk.

Leveraged Loans

(Neutral)

We view leveraged loans more favorably than earlier in the year as increased dispersion and spread widening have improved valuations across portions of the market. While the asset class remains characterized by elevated dispersion and increasingly selective technicals, valuations are becoming more attractive, particularly relative to high yield corporates. CLO demand continues to provide an important source of support, and investor preference remains focused on higher-quality issuers and more resilient sectors.

Software and technology-linked issuers remain an area of caution given ongoing uncertainty surrounding AI-related disruption. However, the broad-based selloff across parts of the sector has also created selective opportunities where market pricing appears disconnected from underlying fundamentals. In several cases, investors have indiscriminately reduced exposure to software and technology credits, creating attractive entry points in higher-quality, mission-critical businesses with durable cash flows, proprietary data advantages, and high switching costs.

More broadly, economically sensitive sectors continue to face pressure from elevated financing costs, inflation uncertainty, and rising input costs, even as overall corporate fundamentals remain relatively stable. CLO issuance and demand for floating-rate exposure remain supportive, helping to offset more mixed retail flows.

Given the improvement in valuations and the growing opportunity set created by elevated dispersion, we have moved to a more neutral stance on the asset class. While selectivity remains paramount, we believe current valuations increasingly compensate investors for refinancing risk and macro uncertainty, particularly in higher-quality segments of the market.

Securitized Product

(Overweight)

Agency mortgage-backed securities (MBS) and non-agency residential mortgage-backed securities (RMBS) remain a high-conviction overweight for 2026. Although agency MBS experienced periods of volatility during May as rates markets adjusted to changing inflation and policy expectations, spreads ultimately retraced much of their widening as demand remained strong and mortgage rates moved off recent highs. Relative valuations across agency MBS continue to appear attractive versus both historical levels and other core fixed income sectors.

Technical conditions remain highly supportive across securitized markets. Demand for high-quality collateral continues to benefit from attractive all-in yields, strong money manager demand, and increasing participation from banks and Government-Sponsored Enterprises (GSEs) as balance sheet constraints ease and relative value improves. At the same time, the Federal Reserve’s measured balance sheet runoff continues to limit net supply pressure. Despite elevated issuance across securitized sectors, spreads have remained well contained, highlighting the strength of underlying demand and market liquidity.

Non-agency RMBS continues to offer one of the more attractive opportunity sets within structured credit. Stable home prices, low loan-to-value ratios, improving collateral performance, and limited refinancing risk continue to support fundamentals. Strong issuance growth has been met with equally robust investor demand, particularly in residential credit sectors where recent vintages continue to demonstrate favorable performance characteristics.

Within CMBS, fundamentals remain resilient, particularly in higher-quality segments. Strong technical demand and improving sentiment continue to support selective opportunities across hospitality, logistics, storage, and high-quality multifamily assets. Issuance across ABS, RMBS, and CMBS markets has remained robust, with many transactions heavily oversubscribed, reinforcing the strength of investor demand despite the higher-rate environment.

We also remain constructive on Danish covered bonds, where defensive characteristics, strong legal frameworks, and attractive USD-hedged yields continue to support relative value.

Featured Insights